China opened the week with a familiar mix of headline progress and deeper structural strain. On the surface, Beijing appears to be making real headway in one of the largest debt cleanups ever attempted. In regional security, Chinese officials took a notably lower-profile approach at Asia’s premier defence forum. At the same time, fresh economic data showed manufacturing momentum fading, while collapsing pork prices offered another reminder that weak domestic demand remains one of the country’s most serious problems.

Taken together, these developments point to the same broader story. China is still managing the consequences of an old growth model built on debt, construction, infrastructure, and export intensity. The authorities can reduce pressure in specific areas. They can swap bad liabilities into more manageable forms. They can stabilise individual markets. They can keep factories moving. But the harder question remains unresolved: how to produce durable growth without relying on the same levers that created today’s imbalances.

Table of Contents

- Debt cleanup is advancing, but the bigger burden is still there

- At Shangri-La, China stayed in the room but not at center stage

- China’s manufacturing sector is still expanding, but momentum is fading

- Pork prices are sending an uncomfortably clear message

- The common thread: balance-sheet repair without demand repair is not enough

- What to watch next

- FAQ

Debt cleanup is advancing, but the bigger burden is still there

Beijing’s campaign to defuse local government debt risks is, at least formally, moving in the right direction. In late 2024, authorities launched a massive debt resolution package worth about 12 trillion yuan, aimed at cleaning up so-called hidden local government debt. This category refers to liabilities accumulated over many years through off-balance-sheet financing structures, particularly those tied to infrastructure-heavy growth and politically driven development targets.

The main tool has been a bond swap programme. Local governments have been allowed to replace expensive, opaque liabilities with lower-cost, longer-dated official debt. The basic logic is straightforward. If a borrower is drowning in high-interest, short-term obligations, replacing those with cheaper and more transparent financing buys time and lowers immediate repayment stress.

On paper, the campaign is producing measurable results. Finance Minister Lan Fo’an has said hidden debt fell by 3.8 trillion yuan in 2024. Officials have also reported that the number of local government financing vehicles on a formal monitoring list has dropped sharply since 2023.

That sounds encouraging, and in one sense it is. A debt swap can reduce rollover risk, cut interest costs, and move liabilities into categories the state can monitor more effectively. If Beijing stays on course, authorities could plausibly declare major success by their mid-2027 target date.

But that is only one layer of the problem.

The more serious issue is the huge pile of operational debt still held by local government financing vehicles, or LGFVs. According to the central bank governor, these obligations reached roughly $14.8 trillion by the end of last year. Unlike hidden debt, this category is not officially treated as direct government debt. In practice, however, local authorities are often still expected to stand behind it.

This distinction matters because it creates a political and financial grey zone. The debts may not sit neatly on government balance sheets, but markets still assume many of them carry implicit state backing. That makes restructuring harder. It also means the debt overhang remains embedded in the system even when the formal statistics improve.

A lot of these liabilities are tied to weak assets, low-return projects, or financing structures that were never especially transparent. Some loans funded projects with little sustainable cash flow. Others were rolled over repeatedly in the hope that future land sales, growth, or refinancing opportunities would solve the problem. Now those assumptions are breaking down.

Land sales, long a crucial revenue source for local governments, remain weak. Restrictions on new borrowing are tighter. Refinancing is not simple, especially when banks are asked to support loans linked to projects that do not obviously generate enough income to justify continued lending.

As a result, some financing vehicles have turned to costly stopgap measures, including high-yield offshore borrowing and expensive funding products used largely to keep up with interest payments. That is not resolution. That is survival.

Asset sales may help, but only if they are used well

To raise cash, local governments are increasingly trying to monetise state-owned assets. These include more traditional holdings such as infrastructure and land resources, but also less conventional assets such as public facilities and even data-related resources.

There is a sensible version of this strategy. If local governments sell or repurpose assets to repay debt or support household income, that can help shift resources away from failed investment cycles and toward balance-sheet repair.

There is also a much less sensible version. If those same assets are simply used to keep unproductive investment models alive, then the sales do little more than delay the reckoning.

That is the central concern raised by critics of the current approach. China can force local governments to absorb part of the adjustment cost. In theory, that is preferable to endlessly socialising losses across the broader economy. But the quality of the adjustment matters. Liquidating assets to unwind bad debt is one thing. Liquidating assets to fund more of the same behaviour that caused the debt buildup is something else entirely.

For a broader look at how energy shocks and financing pressures are interacting with this debt story, see this related China Update News analysis on Hormuz disruption, inflation, and debt strain.

At Shangri-La, China stayed in the room but not at center stage

On the security front, China took a noticeably subdued approach at the Shangri-La Dialogue in Singapore, the region’s most prominent annual defence forum. For the second year in a row, Beijing did not send its defence minister. Instead, the delegation was led by a senior military academic from the PLA National Defence University.

That choice was widely noticed. In gatherings like this, rank matters because access matters. When a defence minister attends, it opens more space for direct exchanges, side meetings, signalling, and crisis management. When a lower-level delegation is sent, it narrows those channels.

The practical effect this year was to give the United States a clearer runway. U.S. Defence Secretary Pete Hegseth had the most prominent platform to present Washington’s security message and engage regional partners.

What was striking, though, was the shift in tone. The American side struck a more conciliatory line toward China than in some previous years, pointing to improved relations after the recent leaders’ summit between Donald Trump and Xi Jinping in Beijing. That softer language was also visible in what was omitted. Taiwan, a staple of previous speeches, was not emphasised in the main address this time.

China’s delegation also avoided the sharper style often associated with these exchanges. There were still warnings about bloc politics and hegemonic behaviour, but the rhetoric was more measured than in prior forums. Chinese representatives spoke in favour of a stable and sustainable military relationship with the United States.

That said, the underlying frictions were never far from the surface.

Chinese officials criticised Japan’s expanding military posture and questioned whether Tokyo could win broad regional trust given its wartime history. They repeated Beijing’s opposition to Taiwan independence. They also raised objections to Australia’s plan to acquire nuclear-powered submarines under AUKUS.

Taiwan remained a central theme in side discussions and panel sessions even if it was less prominent in the headline speeches. Former Chinese ambassador Cui Tiankai argued, in essence, that unification would remove instability from the Taiwan Strait. That argument is not likely to reassure many in the region. A crisis in the strait would almost certainly be one of the most economically and strategically disruptive events in the world, with consequences extending far beyond East Asia.

Some officials from other countries openly criticised Beijing’s decision to send a lower-level delegation, saying China missed an opportunity for direct engagement on the Indo-Pacific’s most pressing security questions. Yet even in partial absence, China remained the organising fact of the conference. Maritime security, defence spending, mobilisation, alliance-building, and strategic competition all revolved around Beijing’s growing power and intentions.

In that sense, China did not dominate the event by presence. It dominated it by gravity.

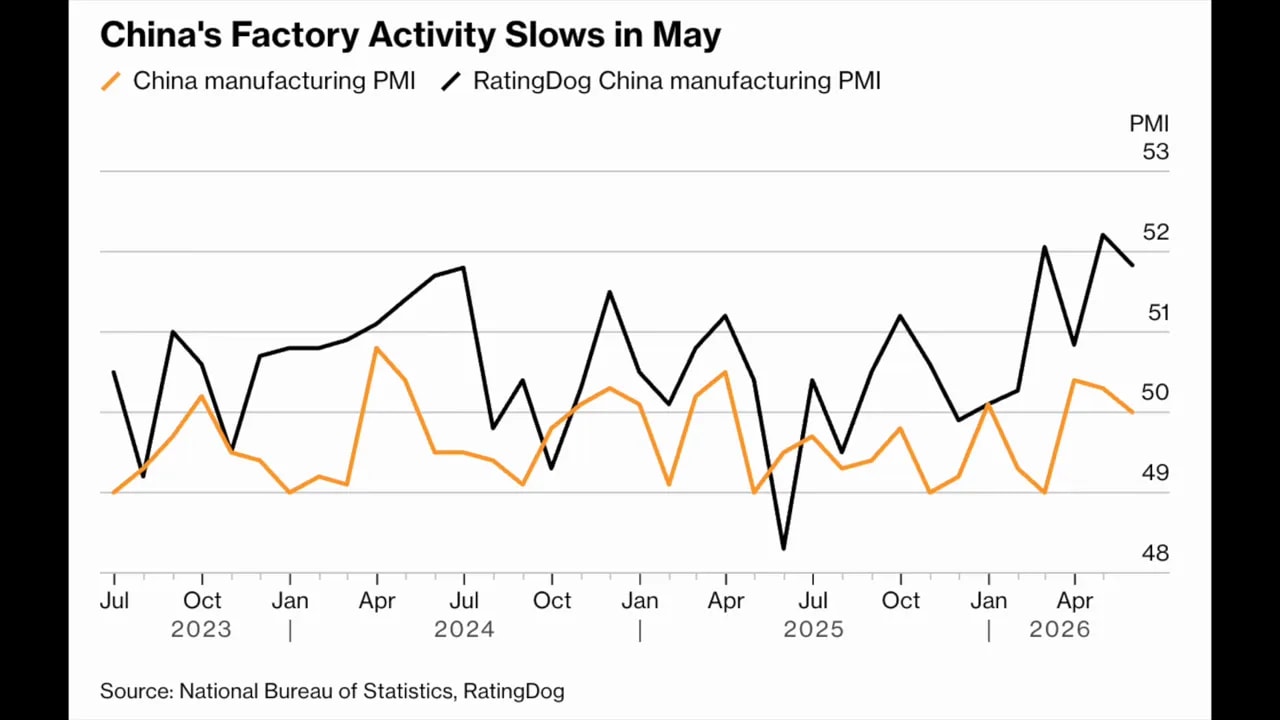

China’s manufacturing sector is still expanding, but momentum is fading

Turning back to the economy, the latest purchasing managers’ index readings suggest that China’s factory sector is losing some speed after a relatively solid start to the year.

The official manufacturing PMI slipped to 50 in May from 50.3 in April. That puts it exactly on the line between expansion and contraction. A separate private survey focused more heavily on export-orientated firms also eased, though it remained in expansion territory.

These are not collapse-level numbers. But they do indicate moderation, and the reasons behind that moderation matter.

One temporary factor was the five-day public holiday, which disrupted production schedules. More persistent pressures are more concerning. Higher energy and transport costs linked to the conflict involving Iran have added strain, especially for smaller export manufacturers already operating on thin margins. Softer global demand has also weighed on activity.

This fits with a wider pattern. Industrial output and retail sales in April were already showing some of the weakest growth rates seen in years. That has renewed calls for more policy support from Beijing, but policymakers face a familiar constraint. The easier it becomes to stimulate through credit and investment, the greater the risk of reinforcing the same debt-heavy growth model that authorities are supposedly trying to move beyond.

And yet China’s export machine is still performing impressively in aggregate. The country posted an enormous trade surplus in 2025, and shipping volumes in 2026 have generally remained above the very strong levels of the previous year.

That resilience is real, but it comes with political costs. Large surpluses intensify trade frictions with major partners. The United States is not the only source of pressure anymore. Europe, too, appears increasingly uneasy about the imbalance between Chinese exports and domestic demand weakness at home. This related China Update News piece on slowing trade momentum and external pressure explores that tension in more detail.

Manufacturers are now looking closely at whether the new U.S.-China trade and investment committees can ease tariff barriers or create some breathing room for exporters. But even if those channels become more productive, they will not solve the deeper issue. China can continue selling to the world at scale, but relying on external demand while domestic demand stays soft is increasingly difficult politically and economically.

Pork prices are sending an uncomfortably clear message

If there is one indicator that captures China’s fragile consumer recovery in unusually vivid form, it may be pork.

Pork is not just another food item in China. It is the country’s most consumed meat, a major part of household diets, and an important component of inflation calculations. Price swings in pork often tell a broader story about the economy.

Right now, that story is not encouraging.

Pork prices have fallen to their lowest level in about 16 years. Over the past four years, prices have dropped by roughly 39 per cent. The immediate drivers are oversupply and weak consumption. The deeper significance is that one of the most basic and politically sensitive consumer markets in the country is still struggling to find equilibrium.

The roots go back to the African swine fever outbreak in 2019, which decimated China’s pig herd and sent pork prices soaring. In response, Beijing pushed for a major rebuilding of supply. Production expanded aggressively. Large-scale farms were constructed. In some cases, even multi-storey pig facilities became part of the effort to industrialise and scale up output.

That strategy worked too well on the supply side. Output recovered and then overshot, creating a glut. At the same time, the broader economy slowed.

The property downturn weakened household wealth and confidence. Consumers became more cautious. Restaurant demand softened. Spending on meals out, a major source of pork consumption, came under pressure. Slower construction activity also reduced demand from another traditional source: construction workers, for whom pork has long been a dietary staple.

So the market is now caught between supply created under old assumptions and demand shaped by a much weaker economic environment.

Smaller farmers are under severe stress, but the pain is not limited to them. Large producers are also seeing profits squeezed. One major pork company reported a sharp drop in annual earnings, and other industry giants have experienced shrinking margins even as they move higher volumes.

The government has tried to stabilise the market. Measures include strategic pork purchases, instructions to local authorities to increase procurement, guidance to cut breeding sow numbers, and stricter weight controls for hogs coming to market. These can help at the margin. They may smooth cycles and reduce immediate pressure.

But they do not fix the core problem. The fundamental issue is demand.

That is why pork has become such a revealing signal. It reflects not just agricultural oversupply, but also sluggish incomes, cautious households, weak confidence, youth unemployment, and the lingering drag from the property sector. China may see temporary inflation from energy costs, but a market as central as pork still points to a deflationary undertone in the domestic economy.

Until households feel secure enough to spend more confidently, pork prices are likely to remain a warning sign rather than a recovery signal. For more on Beijing’s attempts to steady this market, this roundup on pork stabilisation efforts and related economic pressures provides useful context.

The common thread: balance-sheet repair without demand repair is not enough

These four stories may seem separate, but they are closely connected.

- Debt restructuring shows Beijing can reduce financial stress in targeted ways, but large liabilities still remain embedded in local government financing structures.

- Security diplomacy shows China can lower the temperature rhetorically, but the strategic contest in the Indo-Pacific continues to revolve around its power and ambitions.

- Manufacturing data shows the export sector still has strength, but momentum is easing and external demand cannot carry the entire economy indefinitely.

- Pork prices show the domestic demand side remains fragile, despite years of policy effort and periodic stabilisation measures.

That last point may be the most important. China’s old model generated debt through investment and growth targets. The cleanup now underway can contain some of the damage. But if the economy does not rebalance toward healthier household demand, the country risks cycling between temporary fixes and recurring stress.

This is why declarations of success should be treated carefully. Hidden debt can fall while broader quasi-fiscal liabilities remain enormous. PMIs can stay above 50 while growth still cools. Exports can remain strong while domestic confidence stays weak. Pork prices can be stabilised administratively, but only to a point.

The challenge facing Beijing is not simply to manage risk. It is to shift the foundations of growth without triggering a sharper slowdown in the process. That is the balancing act behind much of the current policy mix, and it remains unresolved.

What to watch next

Several indicators will be worth close attention in the coming weeks.

- Whether the local government bond swap programme continues at its current pace and whether Beijing widens support for resolving LGFV operational debt.

- Whether weaker manufacturing data triggers additional policy easing, especially if industrial and retail figures continue to soften.

- Whether U.S.-China economic committees produce any practical tariff relief or remain mostly symbolic.

- Whether pork stabilisation efforts slow the slide in prices or whether weak consumption keeps the market under pressure.

- Whether China’s lower-profile security diplomacy becomes a sustained pattern or a temporary tactical shift.

For now, the picture is mixed but not ambiguous. China is still capable of stabilising pressure points. What it has not yet demonstrated is a convincing path out of the structural weaknesses that created those pressures in the first place.

FAQ

Why is China’s local government debt cleanup being described as progress only on paper?

Because the official campaign is mainly reducing hidden debt by converting it into lower-cost, formal debt. That improves transparency and lowers short-term stress, but a much larger stock of operational debt held by local government financing vehicles still remains. Many of those liabilities are tied to weak assets and uncertain repayment capacity.

What are local government financing vehicles, and why do they matter?

They are entities used by local authorities to raise money for infrastructure and development projects, often outside normal budget channels. They matter because they accumulated massive debts over many years and are central to China’s broader local government fiscal risk.

Why was China’s absence at the top level of the Shangri-La Dialogue significant?

Sending a lower-ranking delegation reduced opportunities for direct engagement with other defence officials and gave the United States more room to shape the forum’s message. It also reinforced concerns among regional actors that Beijing is selective about security dialogue even as its military role in the Indo-Pacific keeps expanding.

Is China’s manufacturing sector contracting?

Not yet, based on the latest PMI data. The official reading stood right at 50, which marks the boundary between expansion and contraction. Private survey data remained above that level as well. The issue is not collapse, but fading momentum driven by holiday disruption, rising costs, and softer demand.

Why do pork prices matter so much for understanding China’s economy?

Pork is China’s most important meat product for consumption and a meaningful component of inflation measures. When pork prices fall sharply for an extended period, it often reflects more than supply conditions. It can also indicate weak consumer demand, low confidence, and broader disinflationary pressure in the economy.

Can Beijing solve the pork market problem through intervention alone?

Only partly. The government can buy pork for reserves, guide herd reductions, and regulate supply conditions. But if households remain cautious and spending stays weak, those supply-side interventions will have limited effect. The underlying problem is still soft demand.

What is the biggest takeaway from this China news update?

China is making tactical progress in several areas, especially in debt management and short-term stabilisation. But the deeper structural challenges remain: weak household demand, heavy local debt burdens, dependence on exports, and persistent strategic tension in the region.