The latest China news cycle captures three big realities at once.

First, Europe is moving away from the old assumption that trade with China can remain heavily imbalanced indefinitely without political consequences. Second, Taiwan is enjoying an extraordinary AI-driven economic surge that is widening the contrast with China’s own slower and more uneven recovery. Third, Beijing is tightening control over strategic sectors and sensitive people, from artificial intelligence specialists to foreign influence concerns.

Taken together, these developments point to a broader shift in the global economic and strategic environment around China. The issue is no longer simply growth. It is control, resilience, industrial competition, and who gets to set the terms of integration.

Table of Contents

- Europe’s China Policy Is Moving From Caution to Rebalancing

- Even Chinese Economists Are Warning That the Export Model Has Become Risky

- The US Foreign Agent Case Shows the Gray Zone in China Influence Concerns

- Taiwan’s AI Boom Is Becoming One of the Biggest Economic Stories in Asia

- Beijing Expands Travel Controls to Private-Sector AI Talent

- What This Week Really Shows

- FAQ

Europe’s China policy is moving from caution to rebalancing.

The European Union is signalling a more serious rethink of its economic relationship with China.

That does not mean Europe is preparing for a rupture. The core message coming out of Brussels is more restrained than that. China remains too important a trade partner for the EU to pursue a clean break. But European officials are increasingly saying something that would have sounded more tentative a few years ago: the current structure of trade and investment is no longer sustainable.

The problem is straightforward. Europe imports a vast volume of Chinese goods while finding it increasingly difficult to expand exports into China. The imbalance is not merely statistical. It is now being felt directly in European industrial sectors that are facing intense competition from Chinese manufacturers, especially in areas where Beijing has spent years building capacity and supporting scale.

European policymakers are under growing pressure to explain why open market access should continue on current terms when Chinese demand for European goods is not keeping pace and Chinese industrial output keeps rising.

The internal European debate is still divided.

Germany remains more cautious, which is hardly surprising given the importance of the Chinese market for German manufacturing, especially autos. Other countries, including France, Italy, the Netherlands, Spain, and Lithuania, are pushing for stronger and broader defensive measures.

What is being discussed is not one single policy but a toolbox. Among the measures under consideration are:

- Stricter procurement rules

- Limits on excessive dependence on any single supplier for critical inputs

- More investment screening

- Greater supply chain diversification

- Sector-specific tariffs or safeguards

- Potential import quotas in highly stressed industries

The sectors most exposed include the chemicals, metals, and clean technology industries. These are exactly the kinds of sectors where Chinese overcapacity, aggressive pricing, and industrial policy support have become central concerns.

European officials are also studying more assertive approaches used elsewhere, including US trade defence tools. The logic is simple enough. If existing instruments are too narrow or too slow, Europe may need stronger options that can operate across sectors rather than one case at a time.

This marks a meaningful evolution in policy thinking. Existing tools such as foreign subsidy rules or carbon border measures have some effect, but they do not fully address the broader structural issue. They are often limited to specific projects or emissions-heavy sectors rather than the entire pattern of imbalance.

For related analysis on Europe’s tougher line, see this China Update coverage of Europe’s trade hard line.

The Risk Europe Is Trying to Avoid

Brussels is not just thinking about economics. It is thinking about political cohesion.

If the EU fails to respond in a coordinated way, member states could try to reclaim more trade authority for themselves. That would risk fragmenting the single market, which is one of the bloc’s main strengths. So this is not only about China. It is also about preserving Europe’s own institutional integrity.

At the same time, the risk of retaliation remains real. Any meaningful European restrictions could prompt Chinese countermeasures. For countries and companies still deeply exposed to the Chinese market, that is a major concern.

So Europe is trying to thread a difficult needle: defend industry, reduce strategic dependence, avoid internal fragmentation, and still preserve some workable commercial relationship with China.

Even Chinese economists are warning. That the export model has become risky.

What makes this moment especially interesting is that concern about the trade imbalance is not limited to Europe.

Inside China, a number of economists and policy voices have begun arguing that the country’s large and growing trade surplus is becoming politically and fiscally costly. The concern is not that Chinese manufacturing has become uncompetitive. Quite the opposite. The concern is that China’s industrial strength is now producing external backlash while domestic demand remains too weak to absorb enough output at home.

One proposed response is selective cuts to export tax rebates.

These rebates have become enormous. They reached roughly US$2.1 trillion in 2025, equal to about 12.1 per cent of annual tax revenue. A large majority of that support appears concentrated in equipment manufacturing. That matters because it helps explain how Chinese producers can remain so aggressively competitive in global markets. If manufacturing sectors are receiving massive direct fiscal support, export performance is being shaped by policy, not just productivity.

The argument from some Chinese policy advisers is that part of this support should be redirected inward. Instead of continuing to heavily subsidise exports, Beijing could use fiscal resources to strengthen domestic consumption through measures such as the following:

- Household subsidies

- Poverty alleviation spending

- Higher rural incomes

- Lower import tariffs

- Policies designed to encourage more consumer spending

The underlying logic is sound. If China wants to reduce trade tensions without giving up industrial capability, it needs a stronger internal demand base. That would ease pressure on external markets and make growth less dependent on pushing manufactured output abroad.

Whether Beijing is willing to make that shift at the necessary scale is another matter. For years, the system has favoured production, investment, and industrial upgrading over household consumption. That model delivered immense manufacturing power, but it also contributed to the imbalances that are now drawing increasingly hard responses overseas.

This broader issue of weakening trade momentum and external pressure is also explored in this analysis of China’s trade engine losing momentum.

The US Foreign Agent Case Shows the Gray Zone in China Influence Concerns

Another development worth noting is the arrest of an American commentator who had worked with Chinese state media and was charged in the United States with acting as an unregistered foreign agent for China.

The allegations are serious. Federal prosecutors say he provided confidential reports to Chinese contacts over a period of years and received around US$100,000 for that work. Investigators also say his travel to the United States was funded by a Chinese contact and that he was encouraged to pursue access to US government institutions.

The case reportedly includes claims that the information was being passed up through Chinese channels at very high levels. At the same time, the accused reportedly told investigators that he refused requests for classified material.

That detail matters because it highlights the murky territory where many influence and intelligence-related cases now sit. Not every activity falls neatly into a classic espionage category. Some involve information gathering, access cultivation, political messaging, relationship-building, or operating in ways that exploit legal and regulatory grey areas.

That ambiguity is part of the challenge for law enforcement. Democracies tend to distinguish between journalism, advocacy, lobbying, informal influence, and covert state-directed activity. But those lines can blur when a foreign state uses intermediaries, media affiliations, or unofficial channels to pursue strategic objectives.

So while this is one case, the broader significance is clear. US concern over Chinese influence operations is not fading. It is becoming more institutionalised, more legally aggressive, and more connected to national security frameworks.

Taiwan’s AI Boom Is Becoming One of the Biggest Economic Stories in Asia

If one side of this week’s China News Update is about pressure and restrictions, the other side is about a remarkable surge in Taiwan.

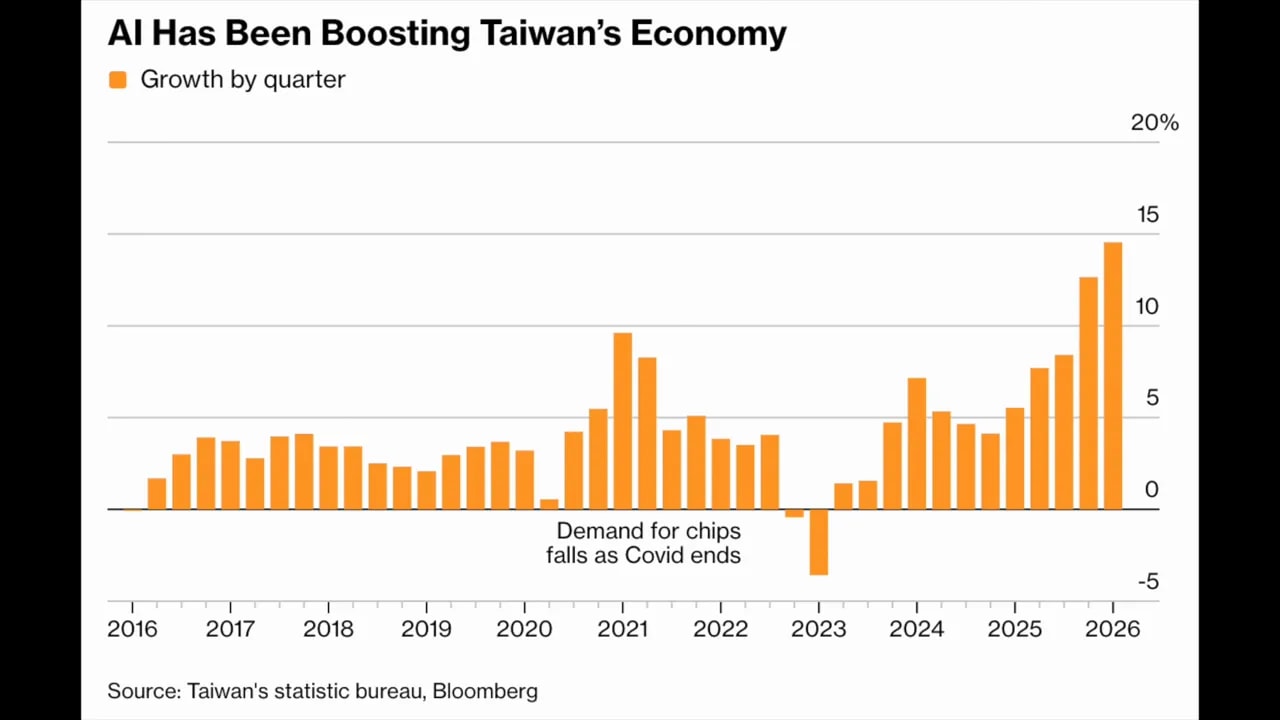

Taiwan has sharply raised its economic outlook for 2026, and the scale of the revision is striking. Official forecasts now point to GDP growth of 9.64 per cent this year, up from an earlier estimate of 7.71 per cent. Export growth is projected at 39.77 per cent, which, if achieved, would be the strongest annual export performance since the mid-1970s.

That kind of number is extraordinary for any economy, let alone a developed one.

The reason is straightforward: artificial intelligence infrastructure.

Global demand for semiconductors, servers, data centres, and advanced hardware has surged far beyond earlier expectations. Taiwan sits at the centre of that buildout because of its dominant position in chip manufacturing. As the AI race accelerates, Taiwan’s companies are capturing a huge share of the upside.

The first quarter numbers underline how strong this wave has become. Taiwan’s GDP rose 14.55 per cent year on year in the first quarter of 2026, the fastest pace since 1981. That is an exceptional result and a reminder that a strategically positioned economy can still produce breakout growth when global demand lines up with its industrial strengths.

TSMC Is at the Center of the Story

No company matters more here than Taiwan Semiconductor Manufacturing Company.

TSMC remains the world’s leading contract chipmaker and a critical supplier for major global technology firms, including Nvidia and Apple. As demand for advanced chips rises, TSMC is capturing not only revenue growth but also investor enthusiasm on a massive scale.

The company’s first-quarter earnings came in at about US$18.2 billion, more than double what it was making two years ago. Its chief executive has also indicated that average profit-sharing payouts to employees will rise by more than 30 per cent this year.

That tells you how deeply this boom is flowing through the system. It is not just lifting exports or market valuations. It is feeding into wages, incentives, investment expectations, and national confidence.

The Stock Market Surge Comes With Concentration Risk

Taiwan also passed India this week to become the world’s fifth largest stock market by total value, reaching roughly US$4.95 trillion.

That is a notable milestone, especially because India’s economy is still far larger in absolute GDP terms. Taiwan’s stock market strength is being driven by a more concentrated but highly strategic exposure to AI hardware, whereas Indian equities have faced pressure from slower earnings growth, higher energy costs, and less direct linkage to the AI buildout.

Still, there is an important caveat. Taiwan’s stock market is extremely concentrated. TSMC alone accounts for roughly 42 per cent of the benchmark index. That is a huge share for a single company. For comparison, even the biggest names in major US indexes represent a much smaller slice.

That concentration creates vulnerability. If sentiment around TSMC or AI hardware weakens, the broader market could feel it quickly. But for now, momentum remains overwhelmingly positive.

Energy Is the Main External Constraint

The biggest obvious weakness in Taiwan’s current growth story is energy dependence.

Taiwan imports around 96 per cent of its energy, which makes it highly exposed to global price shocks. With Middle East tensions pushing up fuel costs, some pressure is already appearing in energy-intensive industries. Industrial production is still rising strongly, but growth has moderated somewhat compared with previous months.

Inflation is another issue to watch. Consumer prices remain relatively contained, though estimates suggest inflation has edged above the central bank’s preferred 2 per cent level. If energy prices stay elevated, discussion around interest rate increases may grow louder.

Even so, the overall picture remains extremely strong. Taiwan is one of the clearest winners of the global AI infrastructure cycle, and that has major implications for regional power, cross-strait politics, and supply chain strategy.

For more on cross-strait dynamics and the wider regional picture, see this related China Update article on Taiwan and broader strategic risk.

Beijing Expands Travel Controls to Private-Sector AI Talent

The final development is one of the clearest signs yet of how Beijing now views top AI workers: not simply as employees, but as strategic assets.

China has expanded travel restrictions to cover elite artificial intelligence professionals working in private firms. Start-up founders, researchers, and executives deemed important to national interests must now obtain government approval before travelling abroad.

This is a meaningful change. Earlier controls focused more heavily on state-owned enterprises and senior government-linked personnel. The new approach extends that logic into the private technology sector, where some of China’s most important AI capabilities now reside.

Major firms affected reportedly include Alibaba and the AI start-up DeepSeek. Importantly, the determining factor is not just job title or employer. Authorities are reportedly identifying individuals based on how strategically important they are judged to be.

That says a great deal about where the Chinese state thinks risk now lies.

In the post-ChatGPT era, top engineers and researchers are increasingly seen as central to national competition. They hold sensitive knowledge, drive key breakthroughs, and can potentially transfer expertise or relationships abroad. From Beijing’s perspective, controlling their mobility is part of protecting technological advantage and reducing the risk of leaks.

But there is another side to this.

Restricting movement may help contain certain risks, yet it can also make talent recruitment and retention more difficult. Highly ambitious engineers often want international collaboration, conference access, and global career options. If they begin to feel boxed in, some may choose to leave earlier in their careers, before they become too strategically important to move freely.

The policy also fits into a broader pattern of tighter controls over foreign influence, overseas investment, and sensitive technology flows. It follows earlier scrutiny connected to the relocation of a Chinese-founded AI company to Singapore, which appears to have sharpened official concern around capital flight, talent mobility, and external linkages.

The message is increasingly unmistakable: in sectors that the state sees as central to national power, private status offers less and less insulation from political control.

What This Week Really Shows

These stories may look separate at first glance, but they are closely connected.

Europe is trying to defend itself against the effects of China’s industrial model. Chinese economists are warning that the export-heavy system is generating too much friction. Taiwan is benefiting enormously from a global technology cycle in which trusted and specialised manufacturing matters more than ever. And Beijing is tightening control over the very people it believes will define the next stage of strategic competition.

That is the real theme running through this China news update.

The contest is no longer just about who grows faster. It is about who can maintain technological advantage, preserve market access, secure supply chains, and keep critical talent under control. Trade, security, industrial policy, and labour mobility are increasingly part of one strategic picture.

For China, that means rising external resistance and tighter internal management at the same time. For Europe, it means deciding how much economic pain it is willing to bear in order to rebalance. For Taiwan, it means extraordinary opportunity, paired with the risks that come from success, concentration, and geopolitical exposure.

None of these tensions are likely to ease soon.

FAQ

Why is the European Union taking a tougher approach toward China now?

The main driver is the growing trade imbalance and the impact of Chinese industrial competition on European sectors. EU officials increasingly believe the current relationship leaves Europe too exposed while offering shrinking access to the Chinese market in return.

Is the EU trying to decouple from China?

No. The current direction is better described as rebalancing rather than full separation. Europe still wants engagement with China, but on terms that reduce excessive dependence and better protect local industries.

Why are Chinese economists discussing cuts to export tax rebates?

Because the trade surplus has become politically sensitive abroad and fiscally expensive at home. Some analysts inside China argue that redirecting support toward household consumption would reduce external tensions and make growth more balanced.

What is driving Taiwan’s strong economic growth?

The main factor is the global boom in AI infrastructure. Taiwan’s semiconductor industry, especially TSMC, is central to producing the chips and hardware needed for that expansion, which has pushed up exports, profits, and market valuations.

Why is Taiwan’s stock market rise significant?

It reflects how much investors value Taiwan’s role in AI supply chains. Overtaking India in stock market capitalisation shows just how powerful that theme has become, even though Taiwan’s economy remains much smaller in overall GDP terms.

Why is China restricting overseas travel for AI professionals?

Beijing increasingly sees top AI talent as strategically important to national security and technological competition. Travel restrictions are intended to reduce the risk of knowledge transfer, talent loss, and foreign influence in sensitive sectors.

What does the US foreign agent case reveal about China-related security concerns?

It highlights how modern influence concerns often operate in grey areas between journalism, commentary, lobbying, access-building, and state-directed information gathering. That makes enforcement more complicated, but it also explains why governments are treating these cases more seriously.