See the Tony Fiddis full video analysis on YouTube. Click here.

Three developments stood out most this week across the Taiwan Strait and the broader China economy.

First, Taiwan has once again moved to the centre of US-China tensions after Donald Trump suggested he may speak directly with Taiwanese President William Lai. That would be a major diplomatic break and one Beijing would see as a serious provocation.

Second, fresh mainland data pointed to deeper economic softness in April, especially in government spending and infrastructure outlays. That is pushing expectations higher that Beijing will have to lean once again on stimulus to keep growth near target.

Third, Taiwan is benefiting enormously from the global artificial intelligence boom. Its stock market has surged, its economy has expanded at a remarkable pace, and firms tied to advanced semiconductor production are becoming even more central to the global technology system.

Taken together, these stories say a great deal about where the region is heading. Taiwan is becoming more economically indispensable at the same time that it is becoming more geopolitically sensitive. Meanwhile, China’s domestic economy still looks unbalanced, with exports and industrial production holding up better than consumption and private demand.

Table of Contents

- US-Taiwan contact is becoming a much more dangerous issue

- The bigger concern: Taiwan becoming a bargaining chip

- Taiwan starts cracking down on AI chip smuggling

- Mainland China’s April data points to a weaker growth picture

- Property still drags, even if a few indicators stabilize

- Why more stimulus now looks likely

- Taiwan’s market is becoming one of the biggest winners of the AI era

- The AI boom is spilling into the real economy

- AMD’s investment is another sign of Taiwan’s central role

- The risks hanging over Taiwan’s success

- What this week really tells us

- FAQ

US-Taiwan contact is becoming a much more dangerous issue

Trump’s latest comments on Taiwan have raised the temperature at a moment when cross-strait tensions are already high. Asked whether he might speak directly with President William Lai, he responded bluntly that he would speak with him and that he speaks to everybody.

That may sound casual, but in diplomatic terms it is anything but casual.

No sitting US president has spoken directly with a Taiwanese president since Washington switched diplomatic recognition from Taipei to Beijing in 1979. The United States has maintained unofficial ties with Taiwan ever since, and it remains Taiwan’s most important security partner and arms supplier. But direct presidential contact has long been treated as a red line issue because of how Beijing interprets sovereignty and legitimacy.

The timing matters as much as the substance. Trump had only recently met Xi Jinping in Beijing, where Taiwan was reportedly one of the central issues discussed. Xi’s warning was stark: if Taiwan policy is mishandled, disagreements could lead to clashes and even war.

Beijing’s message on this point has been consistent for years, but the language has become more explicit and more urgent. Chinese leaders increasingly frame Taiwan not as one issue among many in the bilateral relationship, but as the issue that could determine whether relations remain competitive or tip into direct conflict.

Taipei, for its part, responded carefully. Taiwan’s foreign ministry indicated that Lai would be happy to speak with Trump while also emphasising two familiar points:

- Taiwan’s future should be decided only by its 23 million people.

- Taipei remains committed to maintaining the status quo across the Taiwan Strait.

That cautious language reflects Taiwan’s perpetual balancing act. It wants stronger international support and more visible backing from Washington, but it also knows that high-profile moves can trigger a sharper Chinese response.

The bigger concern: Taiwan becoming a bargaining chip

The deeper problem is not just whether a phone call happens. It is the possibility that Taiwan is increasingly being treated through a transactional lens in Washington.

A proposed US$14 billion US arms package for Taiwan has become a particular flashpoint. Trump recently described the deal as a possible negotiating chip in discussions with Beijing. That remark alarmed Taiwanese officials and many security analysts for a simple reason: deterrence only works when commitments look credible and consistent.

If arms support is framed as tradable, conditional, or available for diplomatic barter, uncertainty grows quickly.

There are now reports that the White House may have temporarily paused the sale, though this had not been formally confirmed at the time of reporting. The stated rationale was the need to preserve US munitions stockpiles during the ongoing conflict with Iran. Even if the pause proves temporary, the signal it sends matters. In Taipei, this reinforces concern that Taiwan’s security needs could become entangled in broader US strategic calculations.

Beijing appears to be pressing that advantage. The Financial Times reported that Chinese officials suggested planned high-level Pentagon visits could be jeopardised unless the arms package is reconsidered. That fits a wider Chinese pattern of using military-to-military engagement as both a pressure tool and bargaining leverage.

For a broader look at how Taiwan risk and weak April data are interacting with China’s strategic picture, see this related analysis.

All of this is unfolding while China continues to intensify military pressure around Taiwan. Chinese aircraft and naval vessels now operate near the island on an almost daily basis. Taiwan’s defence ministry reported multiple Chinese aircraft and ships near its borders within just the previous 24 hours. That kind of operational tempo does not mean war is imminent, but it does increase the chances of miscalculation, exhaustion, and crisis escalation.

The danger in this environment is cumulative. A more transactional US posture, greater Chinese military pressure, and growing symbolic contact between Washington and Taipei each feed into the others. Even if none of these developments alone triggers a crisis, together they make an already dangerous flashpoint harder to stabilise.

Taiwan starts cracking down on AI chip smuggling

Another Taiwan story this week received less attention internationally but is significant in its own right. Taiwanese authorities launched their first major crackdown on AI chip smuggling, seeking to detain three individuals accused of using forged documents to illegally export Nvidia-linked AI servers to China.

The shipment involved only around 50 servers, so this is not a case about massive volume. It is about enforcement, precedent, and signalling.

Taipei is under growing pressure to tighten implementation of US export controls designed to limit China’s access to advanced AI hardware. Taiwan occupies a uniquely sensitive position here. It is central to the global semiconductor supply chain, deeply integrated with US technology restrictions, and also commercially exposed to China.

That makes enforcement politically delicate. But this case suggests Taiwan is taking a harder line on semiconductor security, especially as concerns grow around global chip smuggling networks and the indirect transfer of AI computing capacity.

This is one more example of how the AI race is no longer just about innovation and investment. It is also about customs enforcement, export controls, forged paperwork, and strategic supply chain security.

Mainland China’s April data points to a weaker growth picture

Across the mainland, the economic story this week was one of renewed softness.

April data showed that broad public expenditure fell 7.3 per cent year on year, a steeper decline than the 5.2 per cent drop in March. That marked the fastest pace of contraction in government spending in six months.

That matters because Beijing has increasingly relied on state-led spending to compensate for weak private demand. When fiscal support itself starts to slow, the underlying fragility of the growth model becomes harder to hide.

The pullback in spending coincided with weaker fixed asset investment and subdued consumer demand. Exports have been relatively strong, but the rest of the economy remains far less convincing. Infrastructure-related spending was especially weak, down 17.7 per cent from a year earlier.

Economists offered a few different explanations:

- A temporary funding gap as older projects finished and new approvals had not yet accelerated.

- A policy choice to prioritise repayment of debts owed to firms and local governments.

- A broader sign that fiscal easing is being delivered more cautiously than headline policy statements suggest.

Whatever the immediate reason, the broader pattern is familiar. China’s economy remains highly uneven.

What is working: industrial production, parts of the export sector, and some advanced manufacturing activity.

What is not working well enough: household consumption, confidence, property investment, and the domestic demand side of the economy.

That imbalance has become one of the defining features of the post-property-boom Chinese economy. Consumer confidence remains weak after years of housing stress, falling prices, and soft income growth. Families that once relied on rising property values as a store of wealth are now more cautious. Businesses facing weaker domestic demand are also more reluctant to hire and invest aggressively.

The fiscal spend-through ratio, which measures how much of the funds raised by government actually get spent, also weakened in April. That suggests the policy stance may be looser on paper than in real economic transmission.

Analysts at Huatai Securities warned that reduced fiscal easing could place more pressure on households and companies already facing higher costs from global energy shocks and geopolitical tensions. That is particularly important given the wider uncertainty linked to the Middle East and energy imports. This issue has been explored further in this related piece on China’s fragile recovery and external pressure.

Property still drags, even if a few indicators stabilise.

The property sector, as expected, continued to send mixed signals.

Government revenue from land sales kept deteriorating, which is no surprise at this stage. Land sales are critical to local government finances, so this remains one of the most important structural drags in the system.

At the same time, some property-related tax income improved slightly as home transactions rebounded in several major coastal cities. That is better than outright continued collapse, but it is not the same as a real sector recovery.

This is the distinction that often gets lost in headline coverage. A rebound in transactions in a few large cities can coexist with a much broader national drag from unfinished balance sheet repair, weak developer confidence, and local government financial strain.

The implication is straightforward: Beijing is still searching for a way to stabilise growth without reigniting the old debt-heavy property model. But the alternatives are limited.

Why more stimulus now looks likely

With growth momentum fading, expectations are building that Beijing will step up stimulus in the coming months.

The Politburo has already pledged to accelerate major infrastructure projects across the following:

- Energy networks

- Telecommunications

- Logistics systems

- Water infrastructure

- Computing power capacity

Some estimates put the potential scale of this investment above 7 trillion yuan, roughly US$1 trillion, this year.

The logic is increasingly obvious. If China cannot get consumption growing fast enough, and if external conditions make trade less dependable, then investment once again becomes the default tool for meeting GDP targets.

That is why one of the sharpest observations this week came from Peking University finance professor Michael Pettis, who argued that none of this is particularly surprising. In his view, China can only achieve its growth target if investment keeps growing rapidly, whether or not that investment is economically needed.

China is unable to get consumption growth to accelerate, and with external pressures on its trade surplus, China can only achieve its GDP growth target if it keeps investment growing as fast as ever, whether or not it needs it.

That gets to the core tension in Chinese macro policy right now. Beijing knows the old model produced overcapacity, debt, and diminishing returns. But when growth weakens, it still falls back on the same broad mechanism, especially infrastructure.

With property investment still declining and manufacturing investment affected by intense domestic competition and weak returns, infrastructure spending may be the only large lever left.

For more on that broader pattern of strain, including the property slump and power buildout, see this related China News Update article.

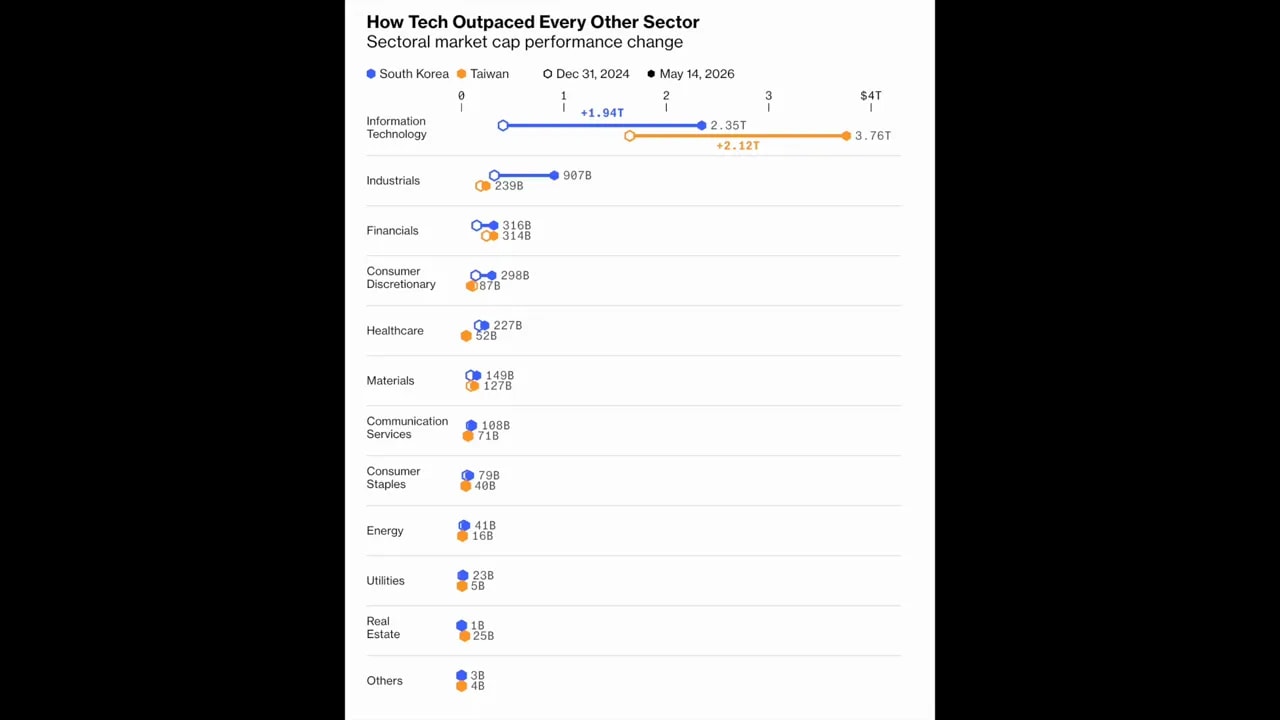

Taiwan’s market is becoming one of the biggest winners of the AI era

While the mainland wrestles with weak domestic demand, Taiwan is riding one of the most powerful global investment themes of the decade: artificial intelligence.

Taiwan’s benchmark stock index has risen roughly 40 per cent this year, helping push the island past both Canada and the United Kingdom to become the world’s sixth largest equity market by total capitalisation.

This rally is not hard to explain. Investors see Taiwanese technology firms, above all TSMC, as essential to the global AI buildout. The chips powering AI data centres, advanced servers, and large language models depend heavily on manufacturing capacity concentrated in Taiwan.

Technology now accounts for nearly 80 per cent of Taiwan’s total market capitalisation. TSMC alone represents close to 40 per cent of the whole market, with a valuation approaching US$2 trillion.

That is a huge advantage, but also a significant concentration risk. Taiwan is benefiting enormously from AI optimism, yet its market is becoming more dependent on a single global narrative: that AI capital spending will remain massive and sustained.

The AI boom is spilling into the real economy

What makes Taiwan’s recent story especially striking is that the technology rally is not just lifting asset prices. It is feeding directly into the broader economy.

Taiwan’s GDP expanded by an astonishing 13.7 per cent in the first quarter, the fastest pace since 1987 and well above expectations. Officials attributed the performance to three factors:

- Surging exports

- Rising investment

- Unexpectedly strong domestic consumption

Exports remain the core of Taiwan’s economy, and more than three quarters of exports are now technology-related. March exports hit an all-time high, jumping nearly 62 per cent year on year as firms around the world rushed to secure AI hardware and semiconductor supply.

There is also a wealth effect at work. As stock prices rise sharply, household confidence and spending can improve as well. That appears to be happening in Taiwan, where retail sales and domestic demand both accelerated in the first quarter.

In other words, the AI story is no longer confined to foundries and server rooms. It is spreading into consumption and the wider economy.

AMD’s investment is another sign of Taiwan’s central role

Another major signal came from AMD, which is preparing to invest more than US$10 billion into Taiwan’s semiconductor industry.

The company plans to deepen partnerships with Taiwanese firms including TSMC and ASE Technology Holdings to develop advanced packaging technologies that are critical for next-generation AI systems. AMD is also ramping up production of its Venice CPU using TSMC’s cutting-edge two-nanometre process.

This matters because the AI supply chain is moving beyond just raw chip fabrication. Packaging, integration, and scaling are becoming just as important. Taiwan’s advantage is that it already sits at the centre of this wider ecosystem, not just one part of it.

That is why so much global capital continues to flow toward Taiwan despite obvious geopolitical risk. For many investors and technology firms, there is still no easy substitute.

The risks hanging over Taiwan’s success

For all the optimism, there are real vulnerabilities.

The first is concentration. Taiwan’s market is increasingly dependent on AI spending continuing at a very high rate. If global technology investment slows, valuations and growth expectations could be hit hard.

The second is energy. Taiwan relies heavily on imported energy, so rising costs linked to conflict in the Middle East create a meaningful economic risk.

The third, of course, is geopolitics. Taiwan can be the biggest winner in the AI hardware boom and still remain exposed to the single largest strategic risk in Asia: conflict or severe crisis in the Taiwan Strait.

That is the core contradiction defining Taiwan’s current moment. It is becoming more valuable to the world economy precisely as it becomes more central to great-power rivalry.

What this week really tells us

Stepping back, the contrast is striking.

Mainland China is still struggling to generate healthy internal demand and appears to be drifting back toward investment-heavy stabilisation. Taiwan, meanwhile, is experiencing a powerful AI-driven upswing in exports, markets, and even domestic spending.

At the same time, Washington and Beijing are handling Taiwan in ways that make the security environment more fragile, not less. A possible direct Trump-Lai conversation, uncertainty around arms sales, and continuous Chinese military pressure all add risk to an already tense strategic environment.

So the picture is not just one of economics or one of security. It is the interaction of both.

Taiwan’s economic importance is rising fast. China’s domestic weaknesses remain unresolved. And the geopolitical framework around the island is becoming more unstable. That combination is likely to shape regional politics and global markets far more than any single headline on its own.

FAQ

Why would a Trump call with Taiwan’s president be such a big deal?

No sitting US president has spoken directly with a Taiwanese president since 1979, when Washington switched diplomatic recognition from Taipei to Beijing. A direct call would break with decades of diplomatic practice and would almost certainly provoke a strong response from Beijing.

Why are analysts worried about the US arms package for Taiwan?

The concern is that military support for Taiwan may be treated as a bargaining chip in broader US-China negotiations. If Taiwan’s defence support appears conditional or negotiable, that can weaken deterrence and increase uncertainty in Taipei.

What was the key weakness in China’s April economic data?

The standout weakness was government spending. Broad public expenditure fell 7.3 per cent year on year in April, and infrastructure-related spending dropped 17.7 per cent. That suggests fiscal support was weaker than many expected, even as domestic demand remains soft.

Is China likely to launch more stimulus?

That is increasingly the expectation. With consumption still weak, property investment still under pressure, and trade facing external uncertainty, Beijing may once again rely on large-scale infrastructure spending to support growth.

Why is Taiwan’s economy growing so quickly?

The main driver is the global AI boom. Demand for advanced chips and related hardware has pushed up exports, investment, and equity prices. Those gains also appear to be feeding into stronger household confidence and domestic consumption.

What are the biggest risks to Taiwan’s current boom?

The biggest risks are a slowdown in global AI spending, higher imported energy costs, and geopolitical instability in the Taiwan Strait. Taiwan’s strength today is tied closely to semiconductors and global technology investment, which makes it both powerful and exposed.