China is facing a dense mix of geopolitical pressure, trade momentum, technology rivalry, and fiscal strain all at once.

On one side, Beijing is navigating a more complicated relationship with both Moscow and Pyongyang as Europe prepares new sanctions tied to Russia’s war effort. On another, China’s trade figures look strong on paper, but much of that strength is being driven by a narrow set of AI-related exports rather than broad-based economic recovery. At the same time, Washington has widened its list of Chinese firms with alleged military links, reinforcing the view that advanced technology is no longer being treated as a normal commercial sector. And inside China, the electric vehicle transition is exposing a less glamorous but very real problem: who pays to maintain the roads?

This is the kind of picture that matters more than any single headline. The details may seem separate, but together they show how China’s economy and strategic position are being shaped by external conflict, internal imbalances, and the growing fusion of commerce, industry, and national security.

Table of Contents

- Beijing’s North Korea diplomacy lands in a more dangerous regional climate

- Europe moves closer to sanctioning Chinese firms linked to Russia

- China’s May trade numbers look strong, but the gains are highly concentrated

- The AI boom is real, but it does not solve China’s structural demand problem

- Washington expands its blacklist of Chinese firms with alleged military ties

- Why the blacklist matters beyond the companies named

- China’s electric vehicle boom is creating a road-funding crisis

- The deeper problem is not just EVs

- What these developments say about China’s current position

- FAQ

Beijing’s North Korea diplomacy lands in a more dangerous regional climate

As Xi Jinping wraps up his visit to North Korea, the trip raises questions that go beyond symbolic diplomacy. One likely objective is to reassess China’s standing with Pyongyang at a time when North Korea appears to have drawn closer to Russia since the war in Ukraine began.

That shift matters for Beijing. China has long been North Korea’s principal backer, but the war in Europe has rearranged relationships. Pyongyang’s deepening links with Moscow create uncertainty over how much leverage China still has and whether Beijing is comfortable with Russia becoming a more influential partner for the North Korean regime.

At the same time, Russia itself has become more dependent on China since the invasion of Ukraine. That has added another layer of tension to Beijing’s calculations. Ukraine’s Volodymyr Zelensky recently called for direct talks with Vladimir Putin and framed Russia as increasingly reliant on China. That puts Beijing in an awkward position. If the battlefield trend continues to shift, China may be pushed to clarify whether it supports diplomacy that could constrain Moscow or whether it remains committed to backing a Russian position more forcefully through its partnerships.

The North Korea trip therefore cannot be read in isolation. It sits inside a broader strategic triangle involving China, Russia, and North Korea, with the war in Ukraine acting as the accelerant.

Europe moves closer to sanctioning Chinese firms linked to Russia

The European Union is preparing a new sanctions package that reportedly includes four Chinese companies accused of assisting Russia’s war effort. The allegations involve support for shipping networks used to dodge existing restrictions, the supply of chemicals with military applications, and components that could be used in drone production.

Even before the company names are formally confirmed, the significance is clear. Brussels is willing to raise the cost for Chinese firms if it believes they are helping sustain Russia’s military capability.

This comes at a delicate moment in EU-China relations. Europe is already in dispute with Beijing over trade, subsidies, and market distortions. European leaders, especially in Brussels, have become more willing to argue that Chinese industrial policy is not just an economic issue but a strategic one. If sanctions tied to Russia are layered on top of anti-subsidy action, the relationship could deteriorate further.

There is still some division inside Europe. Germany, for example, is hardly enthusiastic about subsidised Chinese imports, but it also remains highly exposed to the Chinese market. That split helps explain why Europe’s response often looks more cautious than its rhetoric. Still, the direction of travel is unmistakable.

China has already warned that any additional restrictions will be met with countermeasures. That means the risk is no longer limited to a narrow sanctions dispute. It increasingly looks like one front in a wider economic confrontation.

For a broader sense of how these trade and geopolitical tensions are feeding into China’s economic outlook, it is worth reading this analysis of weak April data and the high-stakes AI race.

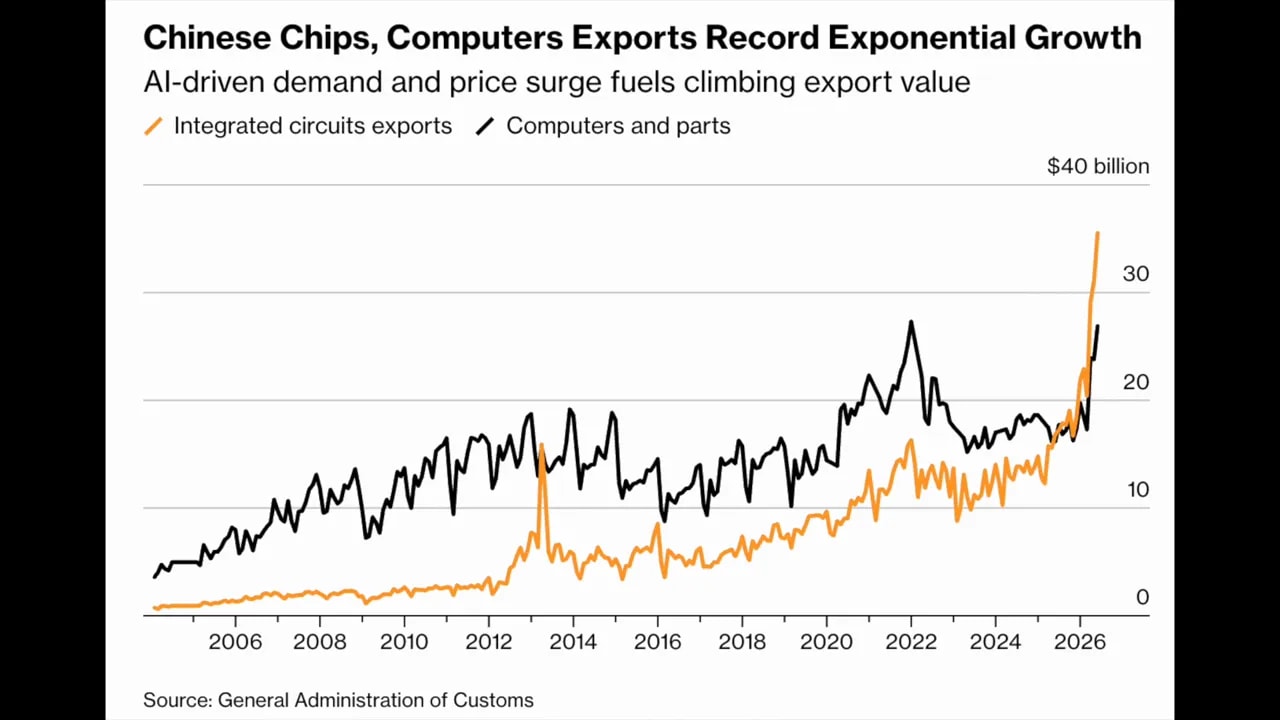

China’s May trade numbers look strong, but the gains are highly concentrated

China’s latest trade data delivered a strong headline result. Exports and imports both rose faster than expected in May, and the country posted a trade surplus of more than $105 billion. The most eye-catching gains came from technology products tied to the global artificial intelligence buildout.

Computers and related components surged. Integrated circuits jumped even more dramatically. That reflects something real: the AI infrastructure boom is creating powerful demand for semiconductors, servers, data centre equipment, optical modules, and supporting hardware. Chinese manufacturers positioned in those supply chains are benefiting.

There was also a likely boost from precautionary orders. In periods of geopolitical uncertainty, overseas buyers often pull demand forward, stocking up earlier to reduce the risk of future disruptions. With instability in the Middle East and persistent concern over trade policy, that probably helped inflate short-term export growth.

Exports to the United States also rebounded sharply, recording their fastest increase in several years. Imports rose strongly as well, helped by higher purchases of foreign chips and advanced equipment. South Korean semiconductor exports to China reportedly soared, reinforcing the point that China remains deeply embedded in regional and global tech supply chains.

But this is where the headline can mislead.

The export strength is not spread evenly across the economy. It is concentrated in a handful of industries connected to AI and advanced electronics. Those sectors are important, but they employ only a limited share of the total workforce and cannot by themselves offset weakness in the rest of the economy.

Traditional sectors continue to face weak demand, severe competition, and ongoing pricing pressure. Consumer sentiment remains soft. That means a surge in chip-related trade does not necessarily translate into broad improvement in household conditions, private business confidence, or local fiscal health.

Another warning sign came from crude oil imports, which fell during the first five months of the year. That suggests softer activity in less dynamic parts of the economy, even as AI-related manufacturing pushes some headline indicators higher.

So yes, the trade data is strong. But it is narrow strength, not economy-wide strength.

The AI boom is real, but it does not solve China’s structural demand problem

One of the most important themes running through the current data is the gap between elite industrial performance and the wider economy.

China has clear momentum in several advanced manufacturing segments. AI hardware, semiconductors, optical modules, and data centre supply chain components are all seeing strong demand. This is good news for firms with the right capabilities and for policymakers who want China to move higher up the value chain.

But this does not mean the country has solved its core economic problem, which is weak domestic demand combined with overcapacity in many traditional industries.

That gap matters because policymakers often point to success in strategic sectors as evidence of resilience. The problem is that these sectors cannot absorb all the pressure elsewhere. If most households are still cautious, if consumer-facing industries remain weak, and if local governments are burdened by debt, then growth in frontier technology can coexist with much broader economic stress.

This is also why trade-led gains can be deceptive. A booming external niche does not automatically repair internal imbalance. In fact, it can sometimes mask it.

That broader issue has shown up repeatedly across recent economic coverage. This related piece on why export-led growth is becoming harder to sustain helps explain why the current model faces deeper limits.

Washington expands its blacklist of Chinese firms with alleged military ties

The United States has released a significantly expanded version of its list of Chinese companies it says are connected to China’s military modernisation. The additions include some of the biggest and most recognisable names in Chinese business, among them Alibaba, Baidu, BYD, Nio, TP-Link, Unitree, and several major solar and technology firms.

This is not a symbolic footnote. It signals how Washington increasingly sees advanced Chinese firms not simply as commercial actors, but as part of a wider national power ecosystem.

Inclusion on this Pentagon list does not automatically trigger sanctions. But it does carry consequences. It can discourage investment, limit access to certain US government opportunities, and put firms under a cloud of heightened scrutiny that may lead to tougher restrictions later.

That is why the additions matter so much. Alibaba is one of China’s most internationally familiar private-sector companies. Baidu is central to China’s AI ambitions. BYD is now a global force in electric vehicles. Unitree is an especially notable addition because it sits at the frontier of robotics and humanoid systems, sectors that are increasingly viewed through a dual-use lens.

In practical terms, the message from Washington is straightforward: semiconductors, AI, robotics, EVs, networking hardware, and biotech are no longer treated as ordinary sectors where economics can be cleanly separated from security.

Beijing rejects these accusations and argues that the United States is weaponising national security to contain China’s rise. But there is also an irony here. China itself has spent years treating advanced technology as a strategic domain, using industrial policy and state planning to build capabilities in exactly these sectors. It is hardly surprising that Washington now responds in similar terms.

The result is a more intense technology war where the room for neutral ground keeps shrinking.

Why the blacklist matters beyond the companies named

The immediate effect falls on the firms added to the list, but the broader impact reaches much further.

- Investors get a signal that political and regulatory risk around Chinese tech is rising.

- Global partners are reminded that supply chains connected to advanced Chinese firms may become more complicated.

- Chinese policymakers receive another incentive to push for self-reliance in chips, AI systems, robotics, and industrial software.

- Foreign governments are likely to face more pressure to align their own technology policies with Washington’s security concerns.

In other words, these moves do not just target particular firms. They contribute to the long-term segmentation of the global technology system.

That is especially relevant because many of the sectors now under scrutiny are exactly the ones powering China’s strongest recent trade performance. So the same industries driving export growth are also the ones attracting the greatest strategic resistance from abroad.

China’s electric vehicle boom is creating a road funding crisis

China’s electric vehicle transition is often presented as a clean industrial success story. There is truth in that. EV adoption has accelerated rapidly, and Chinese manufacturers have become globally competitive at remarkable speed.

But success in one area has created a serious problem in another. The traditional model for funding road maintenance depends heavily on taxes collected from refined fuel products. As more drivers switch from gasoline cars to electric vehicles, that tax base starts to erode.

Meanwhile, the number of vehicles on the road continues to rise.

The numbers are becoming hard to ignore. Estimates suggest China now faces an annual road maintenance funding gap of more than 600 billion yuan. Some assessments indicate that current resources cover only about half of what is actually needed. A large share of ordinary public roads is already underfunded, with many projects formally listed for maintenance but lacking the money to carry out repairs.

The speed of the transition explains part of the shock. New additions to the gasoline vehicle fleet reportedly collapsed from millions in one year to only a few hundred thousand the next, while EV penetration kept climbing. That is excellent for reducing oil dependence and supporting the domestic EV industry. It is much less helpful for a road system still financed through old assumptions.

Authorities are therefore considering new ways to make EV owners contribute more directly to road upkeep. Options reportedly under discussion include:

- Taxes based on mileage traveled

- Charges linked to vehicle weight

- Hybrid models that combine both mileage and weight

- Changes to EV tax exemptions

- Possible taxes tied to EV batteries

Hainan, which has one of the highest EV adoption rates in the country, is already testing a satellite-based mileage charging system linked to navigation tools. That makes it a useful case study for what a future national model could look like.

The deeper problem is not just EVs

Blaming electric vehicles alone would miss the bigger issue.

Even if the roads were still being used mostly by gasoline cars and fuel taxes were flowing more strongly, China would still face a maintenance problem. The deeper structural issue is that the country built an enormous volume of infrastructure without a sustainable long-term funding model to maintain it.

Over the last decade and more, infrastructure construction became a central growth tool. That led to extensive road building, including projects with weak economic returns and toll roads that cannot support themselves financially. Local governments now face heavy debt burdens, and a large share of designated funding is consumed by debt servicing rather than maintenance.

That pressure is visible in toll roads as well, where debt obligations have taken up an overwhelming share of spending while the portion devoted to actual upkeep has fallen sharply.

So the EV transition has exposed the problem, but it did not create it from nothing. It accelerated a collision between two realities:

- China built more infrastructure than many local budgets can sustainably carry.

- The old tax model used to fund that infrastructure is weakening as transport electrifies.

This issue also connects to a wider pattern in the economy. Debt, overcapacity, and the need to maintain assets built during earlier stimulus phases are becoming harder to ignore. For additional context on how fiscal and economic stress is surfacing in different forms, see this piece on China’s stress signals across energy, labour, and AI.

What these developments say about China’s current position

Put together, today’s developments point to four broad realities.

- China’s external environment is getting harder. Between possible EU sanctions, US blacklists, and the ongoing Russia question, strategic pressure is increasing from multiple directions.

- Trade performance is being carried by advanced technology niches. The AI hardware boom is real, but it is not the same thing as broad-based recovery.

- Technology is now inseparable from geopolitics. AI, chips, EVs, robotics, and network infrastructure are all being treated as security issues.

- Domestic fiscal problems are surfacing in practical ways. The road funding shortfall shows how past infrastructure choices are colliding with present economic constraints.

That does not mean China is in immediate crisis. It does mean the margin for easy policy success is shrinking. Strong export numbers can coexist with weak consumption. Industrial ambition can coexist with foreign restrictions. EV leadership can coexist with a collapsing road finance model. This is what a complex transition looks like.

For anyone following China News Update closely, this is the key point: the headline stories are increasingly linked. Trade, security, technology, and fiscal capacity are no longer separate boxes.

FAQ

Why is the EU considering sanctions on Chinese companies?

European officials believe certain Chinese firms may have helped Russia’s war effort through shipping support, chemicals with military applications, or components that can be used in drone production. If confirmed, the sanctions would add another layer of strain to already difficult EU-China relations.

Are China’s latest trade figures a sign of broad economic recovery?

Not necessarily. The strongest gains appear concentrated in AI-related hardware such as chips, servers, and computer components. That is a meaningful source of strength, but it does not automatically indicate healthier demand across the wider economy.

What is the significance of the expanded US blacklist of Chinese firms?

It shows that Washington increasingly views leading Chinese technology sectors through a national security lens. Even without automatic sanctions, being listed can raise investor concerns, limit certain opportunities, and increase the likelihood of future restrictions.

Why are electric vehicles creating a road maintenance funding issue in China?

Much of the traditional funding for road upkeep comes from taxes on gasoline and other refined fuels. As EV adoption rises, those revenues decline, even though road usage continues. That leaves a growing gap unless governments create new charging models.

Is the road funding problem only about EVs?

No. The deeper issue is that China built a vast amount of infrastructure, including some low-return projects, without a durable plan to pay for long-term maintenance. Local government debt and weak fiscal conditions have made that much harder to manage.

What should matter most from this China news update?

The main takeaway is that China’s strongest sectors are also the ones drawing the most foreign scrutiny, while domestic structural problems remain unresolved. That combination is likely to define the next phase of economic and geopolitical pressure.