Photo by zhang kaiyv on Unsplash

A weekend burst of China news brought three very different stories into focus at once.

First, a small propeller aircraft slammed into Beijing’s tallest tower in one of the most tightly controlled airspaces in the world. Second, Alibaba opened a legal fight with the US Department of Defence over its inclusion on a Pentagon list tied to alleged military links. Third, a broader economic picture came into view through a set of six indicators that help explain why China’s growth model is under such visible strain.

Each of these stories matters on its own. Together, they show a country dealing with pressure on security, technology, and the economy all at the same time.

Table of Contents

- Beijing aircraft crash raises immediate security questions

- Alibaba sues the Pentagon over military-linked designation

- The main economic story: China’s growth model is under strain

- 1. The property crisis is still the biggest drag

- 2. Weak consumption and deflation are reinforcing each other

- 3. Demographic decline is no longer a future problem

- 4. The labor market looks weaker beneath the surface

- 5. Exports are still carrying a lot of the load

- 6. The slowdown looks structural, not temporary

- What all of this means for China’s next phase

- FAQ

Beijing aircraft crash raises immediate security questions

A light training aircraft struck the upper floors of CITIC Tower, also known as China Zun, in central Beijing on Friday evening. The building stands about 528 metres tall and serves as a major landmark in the capital’s central business district.

Reports circulating shortly after the crash described shattered glass, falling wreckage, and people below scrambling to get clear of the area. Police and fire crews moved in quickly, sealed off surrounding roads, and restricted access near the tower.

What makes the incident especially unusual is not just the building that was hit but the location. Beijing’s airspace is among the most tightly restricted anywhere. Civilian aircraft do not simply drift over the urban core, especially not near politically sensitive districts. The central business district sits only a short distance from Zhongnanhai, the compound associated with China’s top leadership.

That reality makes the basic question hard to avoid: how did a small civilian aircraft get that far into central Beijing without being intercepted?

The aircraft was identified as a Sunward SA60L, a lightweight two-seat plane commonly used for training. Flight path data reportedly suggested departure from an airfield in Beijing’s eastern Pinggu district before heading west toward the city centre. Local reporting indicated the plane may have belonged to a Beijing flight school, with police later seen outside the school’s premises.

Authorities did not immediately provide a full public explanation. State media was notably quiet in the early aftermath, and online posts and videos appeared to be removed quickly. That information clampdown only intensified speculation.

Several possibilities are likely to be examined by investigators:

- Pilot error

- Mechanical failure

- A navigation or communication breakdown

- A more deliberate or malicious cause

At the time of reporting, casualty details remained unclear. Witnesses described at least one person being taken away by ambulance, and some said they heard a loud blast before debris began falling.

Whatever the final cause, the incident is likely to trigger renewed scrutiny of China’s aviation security controls. In a capital built around layered control systems, an unauthorised penetration of restricted airspace is not a minor issue. It is a serious institutional test.

Alibaba sues the Pentagon over military-linked designation

The second major story came from the technology front. Alibaba has filed a legal challenge in federal court in California after being added to the Pentagon’s Section 1260H list, which names companies the US says are linked to China’s military apparatus.

Alibaba argues the designation was unjustified, lacked sufficient evidence, and denied the company a meaningful chance to respond before publication. According to the filing, the company learned of the move only after the listing was formally released.

This kind of designation does not automatically trigger sanctions. Even so, it carries serious weight. Once a company lands on a Pentagon-linked list of this sort, the practical damage can begin before any formal penalties arrive.

Alibaba says that has already happened. The company argues the designation has interfered with relationships with US-based lobbyists and legal advisers who had previously worked with it. In other words, the consequences are not only political. They are operational and reputational as well.

The broader accusation from Washington is that Alibaba has provided technological support relevant to Chinese military operations aimed at the United States. Alibaba has denied that claim.

A previous report by the Financial Times cited a White House memorandum based on declassified intelligence outlining US concerns, though the underlying evidence was not publicly released in detail.

This case matters because it sits at the intersection of law, national security, and the US-China tech rivalry. It also is not without precedent. Xiaomi previously challenged a similar US designation and was eventually removed from the blacklist. That earlier outcome gives Alibaba at least some reason to fight rather than simply absorb the label.

The lawsuit now puts pressure on the US government to show that its designation can withstand judicial scrutiny. If the evidentiary basis is thin, the case could become awkward for Washington. If the evidence is stronger than what has been publicly disclosed so far, the legal process may expose just how far security concerns around major Chinese tech firms have evolved.

This fits into a much bigger trend. Chinese technology firms operating internationally face an environment where commercial success increasingly overlaps with geopolitical suspicion. Business, data, cloud infrastructure, logistics, semiconductors, and artificial intelligence are now all part of strategic competition.

For related coverage on the widening pressure around trade and sanctions, see this analysis of demographic decline, EU trade friction, and new US sanctions.

The main economic story: China’s growth model is under strain

The biggest story of the day was economic. China is entering a different phase of development, and the change is becoming harder to ignore.

For decades, growth was powered by a familiar combination:

- Rapid urbanization

- Heavy property development

- Export expansion

- A large and still-growing workforce

That formula helped turn China into the world’s second-largest economy and moved hundreds of millions into the middle class. But the old model is losing momentum.

Beijing has lowered its 2026 growth target to a range of 4.5 per cent to 5 per cent, the weakest target seen since the early 1990s. Even that level of growth remains heavily dependent on continued debt expansion, which raises the question of how sustainable the current path really is.

Six broad indicators help explain the challenge.

1. The property crisis is still the biggest drag

China’s property slump remains central to the entire economic picture.

Real estate once contributed roughly a quarter of GDP when related sectors were included. It was not just a construction story. It was a local government finance story, a banking story, a consumer confidence story, and, above all, a household wealth story.

That system began to break down after Beijing moved in 2020 to curb excessive borrowing by developers. Then the pandemic and prolonged lockdowns further damaged confidence. Developers were left with unfinished projects, large debt burdens, and swelling inventories of unsold homes.

Policy support has followed in many forms, including lower mortgage rates, looser purchase rules, and tax incentives. But the market has still not produced a convincing recovery.

Home prices nationwide are estimated to be about 30 per cent below their 2021 peak. That is an enormous destruction of paper wealth, and in China, property has long been the dominant store of household savings.

When households feel poorer, they spend less. When they think prices may keep falling, they delay buying. That is why the property slump is not just another sector downturn. It feeds directly into broader weakness.

For more on how the property downturn continues to affect the wider economy, this China Weekly Update on property stabilisation signs and weak April data adds useful context.

2. Weak consumption and deflation are reinforcing each other

Once property weakens, consumption weakens with it.

Households facing falling home values and uncertain job prospects tend to save more and spend less. That has contributed to one of China’s longest periods of broad deflationary pressure in decades.

Prices have faced sustained downward pressure across housing, vehicles, and many consumer goods categories. On the surface, lower prices may sound helpful. In practice, economy-wide deflation is deeply problematic.

When people expect goods to become cheaper later, they delay purchases. That delay weakens demand further. Businesses then face thinner margins, lower profits, and pressure on wages. The cycle can become self-reinforcing.

Chinese policymakers have increasingly warned about what they call involution, which is essentially destructive price competition. This has shown up in sectors ranging from electric vehicles to food delivery. It is not healthy competition in the classic sense. It is firms under pressure cutting harder and harder to survive.

The deeper issue is that China has spent years trying to boost domestic consumption as a stronger engine of growth. The results remain limited.

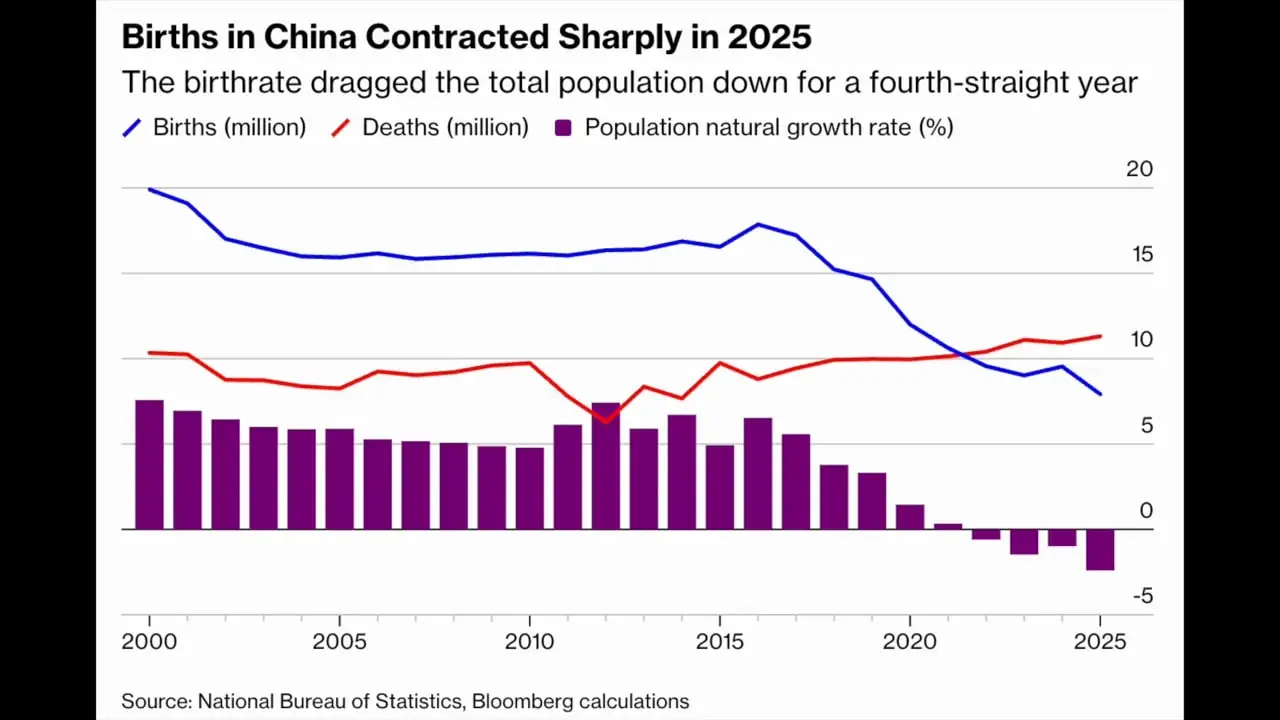

3. Demographic decline is no longer a future problem

China’s demographic shift has moved from warning sign to present reality.

Births fell to 7.93 million in 2025, the lowest level since records began in the era of the People’s Republic. The overall population has now declined for four straight years.

Just as important, the working-age population continues to shrink while the number of retirees rises quickly.

This creates multiple long-term pressures at once:

- Less labor supply

- Fewer new households

- Slower consumer demand growth

- Higher pension and healthcare burdens

- Lower economy-wide productivity momentum over time

Beijing is trying to respond by backing automation, robotics, semiconductors, advanced manufacturing, and artificial intelligence. The theory is clear enough: if there are fewer workers, each worker needs to become more productive.

That may cushion part of the shock. It does not solve the scale of the demographic problem.

If you want a wider look at how demographic pressure is colliding with other policy challenges, this China Update News report on trade momentum and global instability is worth reading alongside it.

4. The labor market looks weaker beneath the surface

Official headline unemployment figures may appear fairly steady, but the deeper labour market picture is much less reassuring.

Youth unemployment remains elevated, especially as record numbers of university graduates enter a softer economy. Many of these graduates are chasing office, services, or technology roles, while a large share of available demand remains concentrated in manufacturing and industrial positions.

That mismatch matters. An economy can have jobs available and still have a weak employment environment if workers do not see those jobs as viable, desirable, or aligned with their training.

Meanwhile, slower wage growth and rising insecurity encourage precautionary saving. Households that feel uncertain about future income do not spend freely.

There is also a forward-looking concern. Rapid progress in industrial automation and AI may improve productivity, but it can also reduce labour demand in specific sectors. That creates an awkward policy balancing act. China needs more productivity, but the very tools meant to deliver it may intensify job anxiety.

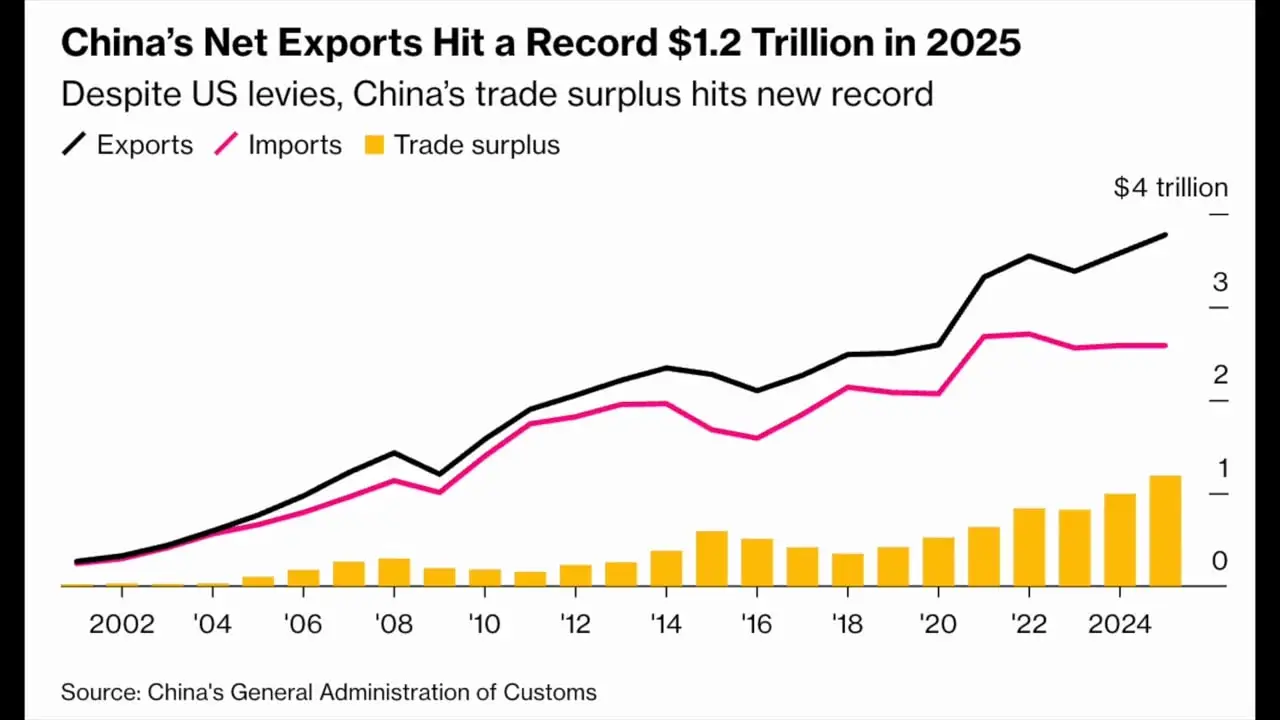

5. Exports are still carrying a lot of the load

One of the clear bright spots in China’s economy has been exports.

Demand abroad for electric vehicles, solar panels, batteries, machinery, and other higher-value products has helped offset domestic weakness. China recorded a trade surplus of roughly $1.2 trillion in 2025, a remarkable figure and evidence of how much the external sector is contributing.

There is also a genuine structural achievement here. Chinese manufacturers have moved further up the value chain. The export mix today is not simply low-cost consumer goods. It includes increasingly sophisticated industrial and technology products.

But relying more heavily on exports introduces its own risks.

The United States, the European Union, and others are growing more concerned about industrial overcapacity and the flood of competitively priced Chinese goods into overseas markets. That concern is already translating into anti-subsidy probes, tariffs, and broader restrictions.

If export dependence rises at the same time foreign resistance hardens, one of China’s few remaining reliable growth supports could become less reliable.

6. The slowdown looks structural, not temporary

This may be the most important point of all.

China’s slowdown increasingly looks structural rather than cyclical. That means it is not simply a matter of waiting for the next rebound.

Part of this is basic arithmetic. It is harder for a very large economy to sustain the kind of explosive percentage growth that was possible when the base was smaller. But the bigger issue is that the old growth drivers are fading all at once.

Property investment is no longer a dependable engine. Urbanisation is maturing. Labour force growth has reversed. Debt has become more burdensome. Consumer confidence remains weak.

Beijing wants newer sectors to take over, including:

- Advanced manufacturing

- Clean energy

- Artificial intelligence

- Biotechnology

- Semiconductors

These sectors have real long-term potential. But they are more capital-intensive and generally create fewer jobs than the property machine they are replacing.

That is the heart of the transition problem. China can become more technologically advanced while still struggling to generate the kind of broad-based household confidence needed for stronger domestic demand.

It still has a formidable industrial scale, world-class infrastructure, and growing technological capability. None of that disappears. The issue is whether those strengths can be converted into a more balanced, durable growth model.

So far, that transition remains incomplete at best.

What all of this means for China’s next phase

The challenge facing policymakers is no longer just how to make growth faster. It is how to make slower growth more sustainable.

That requires more than stimulus. It requires rebuilding confidence among households, stabilising property without restarting the old bubble model, improving job quality, and finding a way to support consumption without leaning endlessly on debt and exports.

That is a very difficult assignment.

China’s era of breakneck expansion is over. The more important question now is what replaces it. If domestic demand does not strengthen meaningfully, the economy is likely to become even more reliant on exports and strategic high-tech industries. That may preserve headline growth for a time, but it also increases external vulnerability and leaves underlying imbalances unresolved.

This is why the latest China News Update feels less like a set of disconnected headlines and more like a snapshot of a system under broad pressure. An aircraft crash in restricted airspace points to uncomfortable security questions. Alibaba’s legal fight reflects a deepening technology and sanctions contest. And the economic data shows a country still searching for a workable post-property growth model.

None of these pressures are likely to disappear quickly.

FAQ

Why is the Beijing aircraft crash considered so unusual?

Because Beijing’s airspace is heavily restricted, especially near politically sensitive areas. A small civilian training aircraft reaching the central business district and striking a landmark skyscraper raises obvious questions about airspace control, flight authorisation, and emergency interception procedures.

What is Alibaba challenging in its US lawsuit?

Alibaba is challenging its inclusion on a Pentagon list of companies alleged to support China’s military. The company argues the move lacked adequate evidence, damaged its business, and was made without giving it a fair chance to respond beforehand.

Does being placed on the Pentagon’s list automatically mean sanctions?

No. The designation does not automatically trigger sanctions, but it can still cause serious reputational and operational harm. It is also widely seen as a possible precursor to tougher restrictions later.

Why is China’s property downturn so important to the broader economy?

Property has been deeply tied to growth, local government revenue, credit expansion, and household wealth. Falling home prices weaken confidence, reduce perceived wealth, and discourage spending, which then spills into broader economic weakness.

What does it mean to say China’s slowdown is structural?

It means the weakness is tied to long-term shifts rather than a temporary dip. The old growth drivers such as property, rapid urbanisation, and labour force expansion are fading, while the newer sectors replacing them do not yet generate the same mix of jobs, demand, and confidence.

Are exports enough to keep China growing?

Exports are helping significantly, especially in electric vehicles, batteries, solar products, and machinery. But relying too heavily on exports creates risk because foreign governments are increasingly responding with tariffs, investigations, and other trade barriers.