“Watch the full Tony Fiddis YouTube video for the complete analysis.”

China is facing a difficult mix of economic weakness at home, strategic uncertainty over Taiwan, and intensifying competition with the United States in artificial intelligence. Taken together, these developments point to a broader story: Beijing still has major industrial strengths, but the foundations of domestic confidence look increasingly fragile.

The latest April data was especially concerning because the weakness was broad-based. Consumption disappointed, industrial output slowed, investment remained under pressure, and credit demand deteriorated sharply. At the same time, comments from US President Donald Trump about Taiwan have raised questions in Taipei and Washington about whether the island could become entangled in a wider US-China bargain. Meanwhile, on the technology front, China is trying to offset chip constraints with something it has in abundance: electricity.

This China news update is less about one isolated headline and more about how several pressures are converging at once.

Table of Contents

- Economic News: April’s data was not just soft; it was broadly troubling

- Industrial output slowed, and investment still depends heavily on the state

- Property remains the biggest structural drag

- The most alarming signal may be collapsing credit demand

- A two-speed economy is taking shape

- The bigger fear: stagnation before prosperity

- Why Beijing is still cautious on stimulus

- Taiwan News: Trump’s comments raise new uncertainty

- Beijing sees opportunity in strategic ambiguity

- AI News: China’s hidden advantage may be power, not chips

- East data, west computing

- Cheap power is becoming a strategic asset

- What ties these stories together

- FAQ

Economic News: April’s data was not just soft; it was broadly troubling

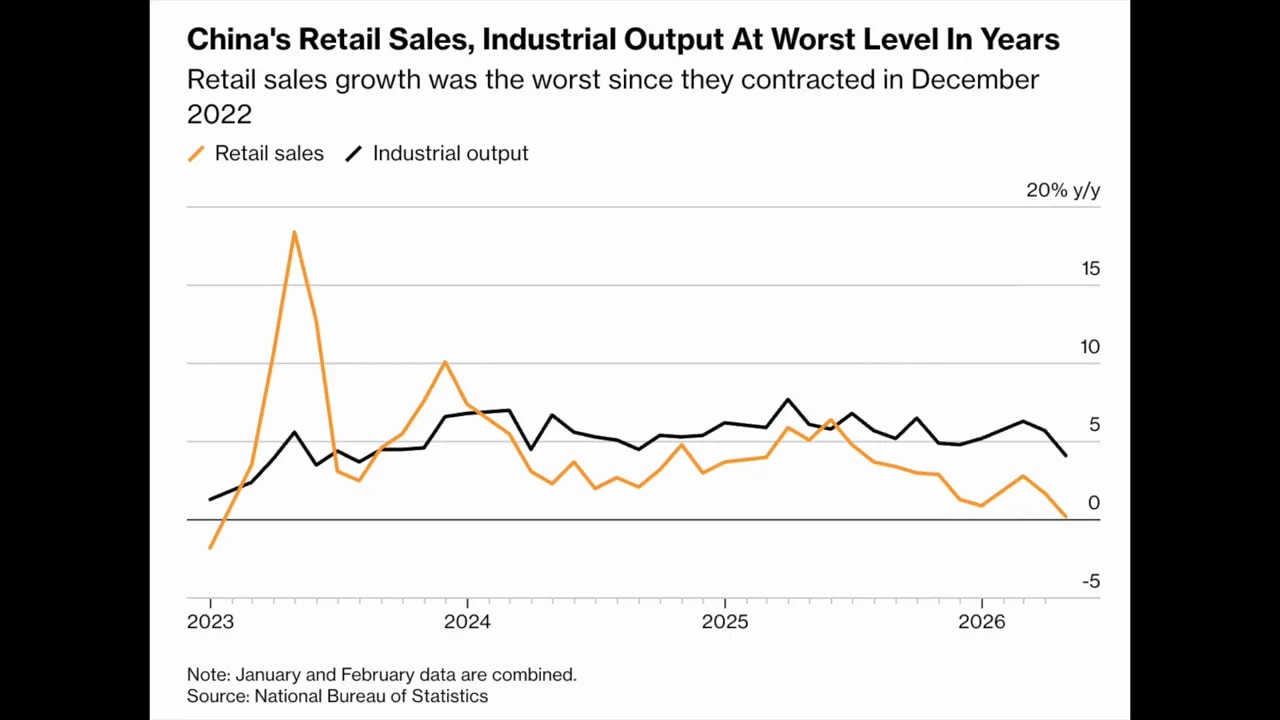

China’s April economic numbers missed expectations across multiple categories, and that matters because simultaneous weakness in consumption, production, investment, and lending is a much more serious signal than a one-off miss in any single indicator.

Retail sales rose just 0.2 per cent year on year in April. Outside the COVID lockdown period, that is one of the weakest readings on record. For an economy that has long talked about rebalancing toward domestic consumption, this is a major warning sign.

Weak consumer spending showed up clearly in discretionary categories. Automobile sales fell 15.3 percent. Furniture and home appliance sales also posted double-digit declines. These are not small cracks. They suggest households remain cautious, wealth effects remain negative, and confidence has not recovered in a meaningful way.

One market observer, writing under the name Shanghai Macro Strategist, argued that investor pessimism around consumption has become deeply entrenched. That looks right. Consumer-related sectors have increasingly underperformed the broader market, and the gap has widened to historic extremes. Put bluntly, many onshore investors appear to want little to do with the consumption story.

That scepticism makes sense in the current environment. If households are worried about jobs, falling property values, and uncertain future income, they are far more likely to save and pay down debt than to spend freely. This is precisely the kind of behavior policymakers have struggled to reverse.

Industrial output slowed, and investment still depends heavily on the state

The weakness was not limited to households. Industrial production growth slowed to 4.1 per cent year on year, the weakest pace in nearly three years. China is still producing at scale, but the pace of expansion is losing momentum.

Fixed asset investment also remained under pressure. In the first four months of the year, it contracted by 1.6 per cent. That is a striking figure for an economy that has long relied on investment-heavy growth.

There was one relatively bright spot: infrastructure investment rose 4.3 per cent, helped by spending on new infrastructure projects. But that strength comes with an important caveat. Infrastructure is one of the few levers Beijing can still pull directly. In other words, it is not necessarily a sign of market-led recovery. It is a sign that the state is still trying to stabilise growth through familiar tools.

That distinction matters. Growth driven by private confidence and household demand is fundamentally healthier than growth sustained by debt-backed administrative spending.

For related coverage on soft April indicators and the broader macro picture, see China Weekly Update: Property Stabilisation Signs, Soft April Data, and AI Momentum.

Property remains the biggest structural drag

If there is one sector that continues to sit at the centre of China’s domestic malaise, it is property. Real estate investment plunged 13.7 per cent during the January to April period, extending the collapse in a sector that once accounted for roughly a quarter of the economy when related industries were included.

The property downturn is not just a sector-specific issue. It hits household wealth, local government finances, private-sector confidence, and credit creation all at once.

For many Chinese households, property has historically been the main store of wealth. When home prices weaken and developers struggle, consumers do not just become less optimistic. They become materially poorer, or at least feel poorer. That directly feeds into weaker consumption.

Local governments are also constrained because they spent years depending on land sales and debt-fuelled infrastructure growth. As those channels weaken, Beijing’s room to stimulate through the old model becomes narrower.

This is why the property story remains so central. China’s economy is not just dealing with a cyclical slowdown. It is dealing with the aftereffects of an exhausted growth model.

For a closer look at the intersection of property weakness, power buildout, and technology competition, see China Property Slump, Power Buildout Surge & Taiwan’s AI Chip Boom.

The most alarming signal may be collapsing credit demand

Perhaps the most worrying part of the latest data was what happened in lending. New yuan lending turned negative in April for only the third time on record.

This is important because weak credit demand tells you something deeper than a weak headline growth figure. It suggests households and businesses do not want to borrow, spend, or invest.

That is a very bad sign for policymakers trying to revive domestic demand. Central banks can make credit cheaper, but they cannot force people to borrow when confidence is low. If households are paying down debt instead of taking on more, and if firms are reluctant to expand, then conventional easing tools become less effective.

It also reinforces the idea that China is drifting toward a more fragile, low-confidence equilibrium. In that type of environment, activity can stagnate even without a dramatic financial crisis.

A two-speed economy is taking shape

One of the most useful ways to understand China right now is as a two-speed economy.

- One China is still growing in export-orientated advanced manufacturing, semiconductors, AI-linked electronics, electric vehicles, and green technology.

- The other China is struggling with weak housing, weak retail, soft construction activity, subdued private investment, and cautious consumers.

This split helps explain why some headline numbers can still look respectable even as domestic sentiment remains poor. Exports and state-backed industrial policy are still generating momentum in selected sectors. But that momentum is not broad enough to repair household confidence or revive the old property-and-consumption engine.

And this imbalance creates new risks. If Beijing becomes even more dependent on exports and industrial overcapacity to sustain growth, it is more likely to intensify trade frictions with the United States and Europe. Complaints about subsidised Chinese exports, from EVs to solar panels and industrial machinery, are already mounting.

That means China’s domestic weakness can increasingly spill outward into geopolitical and trade tensions.

The bigger fear: stagnation before prosperity

The darker scenario is not necessarily a sudden collapse. It is prolonged stagnation.

Analysts increasingly worry that China could slide into something resembling Japanese-style stagnation: weak demand, deflationary pressure, falling asset prices, and declining private-sector confidence. But there is a crucial difference. Japan entered its stagnant period as a rich, advanced economy. China, in per capita terms, is still much poorer.

That would make a long period of low growth much more painful socially and politically.

Youth employment is a key pressure point. Weak consumption and weak private investment are a bad combination for labour demand, especially when millions of graduates enter the workforce every year. There are already widespread concerns that even top students from elite universities are anxious about post-graduation job prospects.

That matters because confidence is not just about current income. It is about future expectations. If the most educated young people are increasingly uncertain about their prospects, that feeds back into savings behaviour, household caution, and broader pessimism.

Why Beijing is still cautious on stimulus

Given the weakness in the data, many would expect a large stimulus response. But Beijing appears reluctant to launch another massive package.

There are several reasons for this caution:

- Debt levels are already very high.

- Local governments remain heavily burdened.

- Higher global energy prices have complicated the inflation outlook.

- Officials likely want to avoid repeating the debt-heavy excesses of previous downturn responses.

Some limited easing is still possible, including reductions in banks’ reserve requirement ratios. But the broader message from authorities appears to be one of restraint, at least for now.

That restraint may prove costly if confidence continues to deteriorate. At some point, the challenge will no longer be simply meeting an annual GDP target. It will be confronting a structural economic model that is increasingly reliant on exports and state-backed industry while domestic demand remains weak.

And that is the really uncomfortable reality. The world’s second-largest economy still does not have enough healthy internal demand to comfortably sustain itself.

Taiwan News: Trump’s comments raise new uncertainty

The second major development concerns Taiwan, where remarks by US President Donald Trump have triggered concern that the island could become a bargaining chip in broader negotiations with Beijing.

After his summit with Xi Jinping, Trump said official US policy had not changed. But several of his comments still raised eyebrows. He said, “I’m not looking to have somebody go independent,” and added that the United States is “supposed to travel 9,500 miles to fight a war.” He also described a proposed arms package for Taiwan as “a very good negotiating chip for us", saying, “I may do it; I may not do it.”

That language immediately unsettled officials in Taiwan. The concern is straightforward: if support for Taiwan becomes folded into a wider US-China deal, deterrence could weaken even if formal policy language stays the same.

The timing is particularly sensitive. Taiwan has already allocated funding for billions of dollars in previously approved US weapons purchases, and lawmakers have been preparing financing for another large package reportedly awaiting White House approval.

Taiwan’s response has been to restate a long-standing position. President Lai Ching-te emphasised that Taiwan is already sovereign and “not subordinate” to the People’s Republic of China. He also argued there is “no issue of Taiwan independence", reflecting Taipei’s position that the Republic of China already functions as an independent state.

Lai also highlighted Taiwan’s central role in global semiconductor supply chains. That point is not rhetorical. Taiwan produces around 90 per cent of the world’s most advanced chips, a reality often described as the island’s “silicon shield". Any disruption in the Taiwan Strait would reverberate through Indo-Pacific security, global manufacturing, and the world economy.

For additional background on Taiwan-related regional risks and strategic pressures, see this analysis on debt strain, inflation pressure, and rising Taiwan blockade planning.

Beijing sees opportunity in strategic ambiguity

Chinese officials appeared encouraged by Trump’s wording, particularly his opposition to Taiwanese independence. State media quickly used the comments to reinforce a familiar domestic message: that the United States cannot ultimately be trusted to defend Taiwan.

That narrative serves Beijing well. If Washington appears hesitant or transactional, Chinese policymakers can use that both externally and internally. Externally, it can sow doubt in Taipei. Internally, it strengthens the argument that time and pressure are on Beijing’s side.

At the same time, it is worth noting that not everyone sees these remarks as a major policy shift. Some analysts argue that too much is being read into them and that formal US policy remains unchanged. Trump’s ambassador to Beijing insisted that Washington does not support independence but also does not want to see coercion across the Strait and still wants a peaceful solution.

That leaves the situation in a familiar but uncomfortable place: ambiguity. The most immediate test will be whether the White House ultimately approves the arms package. That decision will be watched very closely in Taipei, Beijing, and across the Indo-Pacific.

AI News: China’s hidden advantage may be power, not chips

The third major story is the AI race, where China still trails the United States in cutting-edge semiconductors and frontier large language models. But Beijing is pushing hard in a different area that may prove strategically decisive: electricity.

Over the past decade, China has built the world’s largest power grid and massively expanded electricity generation across coal, nuclear, hydro, solar, and wind. Between 2010 and 2024, China added more new power generation capacity than the rest of the world combined. Last year it produced more than twice as much electricity as the United States.

That matters because AI is not just a software race. It is increasingly an infrastructure race.

Training and running large AI systems requires vast amounts of energy. Data centres, advanced computing clusters, and chip-heavy processing all need reliable and affordable electricity. China’s policymakers clearly understand this and are now trying to turn energy abundance into an AI advantage.

East data, west computing

A key part of this strategy is Beijing’s “East Data, West Computing” initiative, launched in 2021. The idea is simple: move energy-intensive AI and cloud computing workloads away from crowded eastern cities toward western and northern regions where land is cheaper and renewable energy is more abundant.

Regions such as Inner Mongolia have become central to this effort. Wind turbines, solar farms, transmission lines, and data centre clusters are being built at scale. Some cities are being rebranded as cloud hubs, with more than 100 data centres either operating or under construction.

The long-term goal is a nationwide compute network linking hundreds of data centres into shared AI infrastructure by 2028.

This gives Chinese firms a partial workaround for US semiconductor restrictions. If domestic chips are less powerful than top-end American ones, companies can still compensate by networking larger numbers of processors together. That is less efficient, but if electricity is cheap and available, it becomes far more viable.

Cheap power is becoming a strategic asset

Companies such as Huawei, Alibaba, and Baidu are relying on large-scale processor clusters to keep pace in AI development. That requires enormous power demand. Cheap electricity therefore becomes more than an economic input. It becomes a strategic asset.

This also helps explain how Chinese firms like DeepSeek have been able to develop competitive AI models at a comparatively lower cost than some Western rivals. Cost control in AI does not only come from software optimisation. It also comes from cheaper compute infrastructure and cheaper power.

Meanwhile, the United States is confronting what some technology executives have started calling an “electron gap". The concern is that ageing grids, slow approvals, and infrastructure bottlenecks could limit America’s ability to expand AI capacity quickly enough. Morgan Stanley estimates that US data centres could face a 44-gigawatt electricity shortfall within three years.

Beijing is trying to move the other way. Several major agencies, including the National Development and Reform Commission and the National Energy Administration, have rolled out an AI-and-energy action plan aimed at tightly integrating AI development with the energy sector. Targets include more clean energy supply for AI infrastructure by 2030 and the construction of gigawatt-scale computing hubs directly connected to dedicated power systems.

The strategic point is clear. In the next phase of the global AI race, the key bottleneck may not be chips alone. It may be about whether a country can generate and deliver enough electricity to support large-scale computing.

What ties these stories together

At first glance, weak retail sales, Taiwan ambiguity, and AI electricity policy may look like separate issues. They are not.

All three point to the same underlying reality: China is trying to manage a transition from one era to another.

- The old property-heavy domestic growth model is struggling.

- External demand and industrial policy are becoming more important.

- Technology competition with the United States is increasingly about systems, infrastructure, and strategic resilience.

- Geopolitics is becoming more tightly connected to economics and supply chains.

That transition could still produce areas of impressive strength. China remains formidable in manufacturing scale, industrial coordination, and now, increasingly, power infrastructure. But the domestic side of the economy remains the weak link, and that weakness carries political, social, and strategic consequences.

This is why the latest data deserves close attention. It is not just a bad month. It is another sign that China’s biggest challenge may no longer be how to grow fast, but how to restore confidence in a system where households, businesses, and local governments all appear increasingly cautious at the same time.

FAQ

Why were China’s April economic figures seen as especially weak?

Because multiple key indicators deteriorated at once. Retail sales nearly stalled, industrial output slowed to its weakest pace in years, fixed asset investment contracted, property investment plunged, and new yuan lending turned negative. That combination suggests deeper fragility rather than a temporary soft patch.

What is the biggest structural problem in China’s economy right now?

The property downturn remains the central structural drag. It weakens household wealth, suppresses consumption, strains local government finances, and undermines business confidence. Since property once played such a large role in the economy, its prolonged slump has broad spillover effects.

Why is negative credit demand such an important warning sign?

Because it suggests households and businesses do not want to borrow even when policymakers are trying to support growth. That points to weak confidence. If people are paying down debt instead of spending or investing, monetary easing becomes less effective.

What did Trump say about Taiwan that caused concern?

He said he was not looking to have “somebody go independent", questioned the idea of travelling 9,500 miles to fight a war, and described a proposed Taiwan arms package as a “very good negotiating chip". Those remarks raised concern that Taiwan could become part of a broader bargain with Beijing.

Has US policy on Taiwan formally changed?

Publicly, no. US officials have maintained that policy remains unchanged: Washington does not support Taiwan's independence, opposes coercion, and wants a peaceful resolution. The concern is more about tone, signalling, and how Beijing and Taipei interpret ambiguity.

How is China trying to compete in AI despite US chip restrictions?

One major advantage is electricity. China has built enormous power generation and transmission capacity, allowing firms to run large clusters of less advanced chips. That can partly offset restrictions on access to top-end American semiconductors.

What is “East Data, West Computing”?

It is a Chinese strategy to shift energy-intensive data processing and AI computing from dense eastern cities to western and northern regions with cheaper land and abundant power, especially renewable energy. The goal is to create a nationwide computing network that supports AI development at scale.

Why does electricity matter so much in the AI race?

Because advanced AI requires vast data centres, heavy computing loads, and constant processing power. As models scale up, electricity becomes a major bottleneck. Countries that can provide abundant, reliable, and low-cost power will have a growing advantage in AI deployment.

This China news update ultimately highlights a difficult balancing act. Beijing still has scale, industrial capacity, and strategic direction in key sectors. But domestic demand remains weak, external tensions remain high, and future growth is increasingly tied to whether China can navigate structural economic strain while competing in a far more contested global environment.